Australian housing market turnover - the RBA's nine chart insights

GUEST OBSERVER

Housing market turnover is defined as transactions in the housing market involving the transfer of ownership.

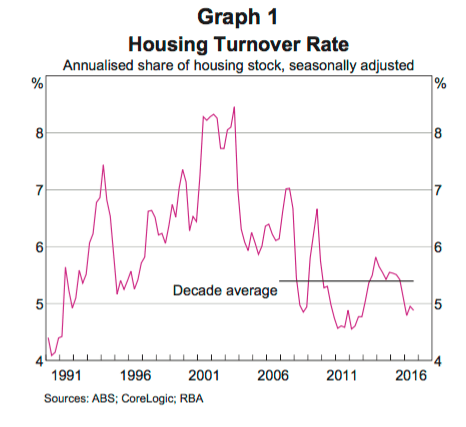

After rising for a number of years, the rate of housing turnover (that is, the number of transactions relative to the stock of housing) has trended lower since the early 2000s (Graph 1). The most recent decline in the turnover rate has been unusual, particularly given the strength in other indicators of national housing market activity, such as housing prices.

The rate of housing turnover helps inform assessments of conditions in the housing market and can also influence broader economic conditions. To the extent that housing transactions are financed by debt, the value of housing turnover will be closely related to the value of housing loan approvals and subsequently housing credit growth.

Changes in the housing turnover rate can directly affect income and employment in related industries, such as real estate services and other professional services, and have spillover effects on household spending through various indirect channels. Tax paid on the transfer of property ownership is also a key source of state government tax revenue.

The Australian Bureau of Statistics (ABS) also reports housing turnover (‘transfers’) using CoreLogic’s unit-record database. The ABS does not adjust for missing observations and as a consequence its measure of housing turnover is typically lower than CoreLogic’s, although upward revisions to the ABS data tend to bring the series closer together over time.

Drivers of Housing TurnoverNot surprisingly, the reasons for moving differ by age. Older owner-occupiers (aged 55 years and above) more commonly cite downsizing and location, whereas those aged 35 to 54 years are more often buying larger or better properties. Younger home owners (aged 18 to 34 years) appear to be the least concerned with the location of the home and more frequently prioritise having their own place and family and friends in their moving decision.

Moving for work is not a common reason for buying a home, regardless of age, which might reflect a view by some households that work is a temporary reason for moving and therefore not sufficient to commit to home ownership.

While the reasons for moving have not changed much over time, the HILDA Survey shows that households are moving less often than they were in the early 2000s (Graph 2).

The largest declines in moving frequencies that involve the transfer of ownership have been for renters transitioning to owner-occupiers and then owner-occupiers moving between dwellings. Even when controlling for various demographic and income characteristics which may affect the decision to move, the probability of owner-occupiers having moved in the previous year appears to have declined since the early 2000s, particularly if owner-occupiers were renters in the previous year.

The factors that affect the propensity of households to move, and therefore housing turnover, are closely related to the drivers of home ownership, which are explored in detail in RBA (2015). For example, the consequences of disinflation and financial deregulation included a significant increase in many households’ borrowing capacity during the late 1990s and early 2000s.

This likely contributed to relatively high rates of housing turnover in that period. On the other hand, financial and other costs can discourage households from moving frequently, particularly when the purchase of a home is involved.

Demographics are another important factor affecting home ownership and housing turnover.

Regression analysis suggests that being in a relationship increases the probability of transitioning from being a renter to an owner-occupier and the probability of transitioning between dwellings as an owner-occupier.

The magnitude of the effect is much larger for the former transition, suggesting that people are inclined to wait until partnering before purchasing a home. Higher incomes and higher levels of education are also particularly important factors that increase the probability of transitioning from renter to owner-occupier.

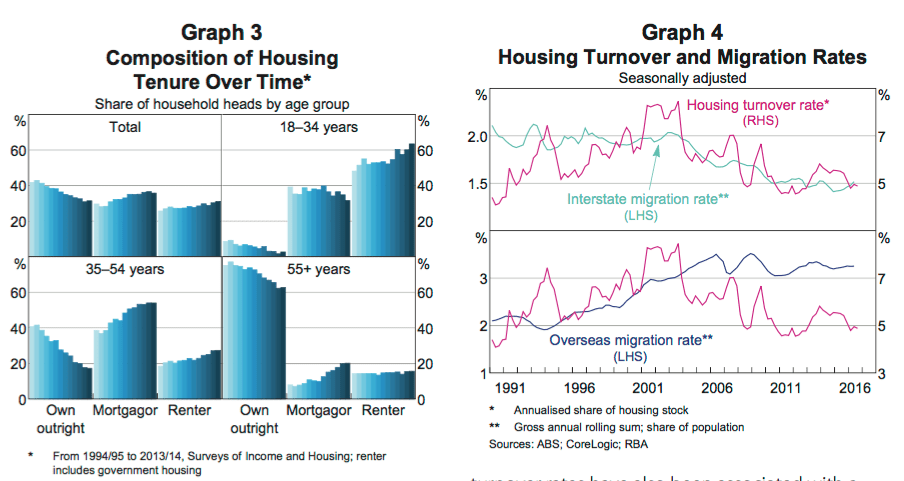

Another demographic factor potentially affecting housing turnover is the age composition of home owners. Data from the ABS Survey of Income and Housing show a small increase in the aggregate share of renter households, driven largely by households with a household head aged under 55 years (Graph 3). All else being equal, a larger proportion of renter households would be expected to reduce housing turnover, to the extent that turnover measures home sales as opposed to household moves.

Given that renters tend to be disproportionately younger households, this suggests that older owner-occupier households represent a larger share of housing turnover than in the past. If these older households have a tendency to move less frequently (for example, because of more stable employment, established social networks and a preference to age in their own homes), this could imply a potentially lower equilibrium rate of housing turnover (Olsberg and Winters 2005).

Another driver of housing turnover is migration, to the extent that households moving between states or countries are purchasing or selling homes. The decline in the turnover rate since the early 2000s appears to have been associated with a significant decline in the rate of gross interstate migration (Graph 4).

As previously discussed, the decision to move reflects an interaction between various benefits and costs. For example, moving interstate may bring households closer to family and friends or better employment opportunities, but can involve high costs. Structural factors such as improvements in technology and the changing nature of work are likely to have reduced the benefits of interstate migration while increasing insecurity around employment and income, which would be expected to weigh on the housing turnover rate (Bachmann and Cooper 2014; Kaplan and Schulhofer-Wohl 2015; RBA 2015). In the United States, lower housing turnover rates have also been associated with a long-run decline in interstate migration, which in turn has been linked to declining labour mobility (Molloy, Smith and Wozniak 2014).

By contrast, the relationship between rates of housing turnover and gross overseas migration (the sum of overseas immigration and emigration) appears to have been less strong. The increasing housing turnover rate during the 1990s and early 2000s was associated with a rise in the rate of gross overseas migration, although the decline in the turnover rate since then has occurred alongside a relatively high gross overseas migration rate.

While higher rates of gross overseas migration would be expected to have a positive effect on the housing turnover rate, this relationship could operate with a lag given that a large proportion of new immigrants tend to rent their first home in Australia before later transitioning to home ownership (Khoo et al 2012). Students also comprise a large share of new migrants to Australia and are likely to be less able and inclined to purchase housing than the average household (RBA 2015).

Housing Turnover and the Recent Increase in Apartment Building

The decline in the national housing turnover rate in recent years has occurred despite strength in a number of housing market indicators such as national housing price growth, which has historically been positively correlated with the turnover rate. While the previous section outlined some potential reasons for the longer-run decline in the housing turnover rate, part of the recent weakness could be due to measurement issues arising from the increased share of apartments in new housing construction.

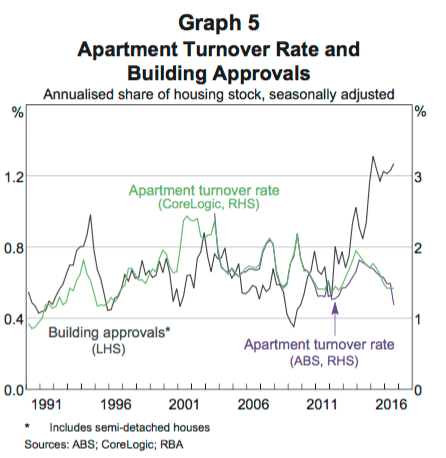

Private residential building approvals for higher- density housing have increased sharply since 2009 and now account for around half of all approvals (Graph 5). Meanwhile the apartment turnover rate, which has historically moved in line with building approvals, has declined. Evidence from business liaison suggests that the majority of new apartments are purchased off-the-plan, well before construction has commenced, and that off-the-plan sales have settlement lags of around two or three years (Shoory 2016).

However, data providers have limited information about these sales until settlement, implying that contract-dated measures of housing turnover are likely to be understating actual turnover in the most recent years. Elevated levels of new apartment construction would be expected to increase the degree of this understatement.

One way to approximate the extent of the understatement of apartment turnover is to estimate the share of turnover that relates to new apartments versus existing apartments. This information can then be used to adjust the most recent data. The ABS and private research companies publish data on house and apartment turnover separately but are not able to disaggregate turnover by new and existing housing. We use the number of higher-density building approvals as a proxy for new apartment turnover and estimate the turnover of existing apartments as a residual. In doing so, we assume that the approval and contract dates are equivalent and that all approved construction is completed. This seems to be a reasonable proxy for new apartment turnover given that a large proportion of new apartments are sold before being built and housing turnover is measured at the contract date of the sale.

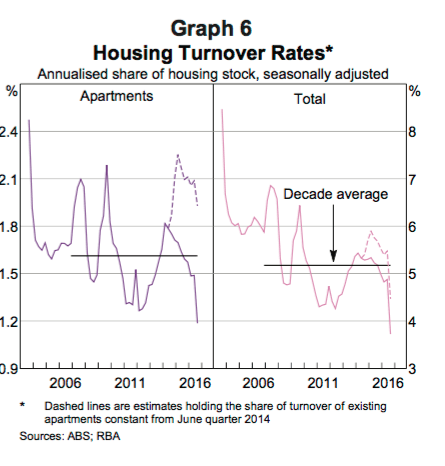

The recent sharp increase in higher-density building approvals seems to imply that turnover of existing apartments has fallen significantly since 2014 to around zero (when estimated as the ABS measure of total apartment turnover minus higher-density building approvals). This seems unlikely, suggesting that total apartment turnover is understated. We can estimate the effect of the understatement by adjusting existing apartments’ share of turnover to more reasonable levels. For example, keeping the share constant from the June quarter 2014 (at around 18 per cent) and scaling up the volume of total turnover implies that the actual apartment turnover rate may be around 1⁄2–3⁄4 percentage point higher than reported over this period (Graph 6). Under these assumptions, apartment turnover appears to have increased sharply through the second half of 2014 and early 2015, before declining to around 2 per cent of the housing stock. The aggregate housing turnover rate would have also increased through late 2014 and early 2015 under these assumptions, before declining to be below its decade average rate.10

Although CoreLogic publishes modelled estimates of housing turnover, the pattern of revisions to these data over recent years suggests that the estimates have not been fully adjusted for the increased share of off-the-plan sales. For example, upward revisions to apartment turnover have been substantial for several years after the data were first released. By contrast, revisions to house turnover tend to be limited after a few months. Scaling up reported apartment sales from mid 2014 onwards by CoreLogic’s average ttwo-year revision rate produces similar estimates to the above exercise.

Implications for Economic Activity

Developments in the rate of housing market turnover can affect broader economic activity through several channels. A number of occupations are involved in housing transactions; these include real estate agents, lawyers and finance professionals. A decline in the rate of housing turnover would be expected to generate less employment and income growth for these professions at the margin.

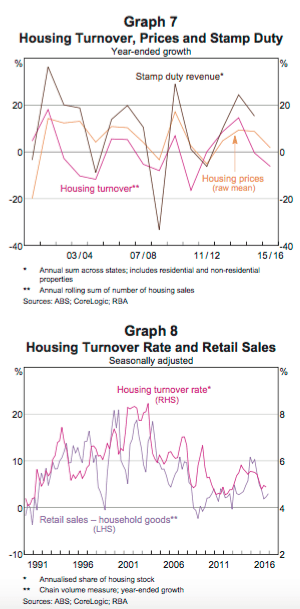

Housing turnover also affects property tax revenue, which accounted for about 40 per cent of total state tax revenue in 2014/15.11 More than half of property tax revenue is typically derived from tax paid on the transfer of property ownership (stamp duty). All else being equal, a decline in the number of housing transactions would be expected to reduce stamp duty revenue. However, given that stamp duty is calculated as a proportion of the sale price of the property, strong growth in national housing prices can more than offset a decline in turnover, as occurred in 2014/15 (Graph 7). The interaction between housing turnover and price growth, as well as state differences in the rate of property taxation, concessions and surcharges, can therefore affect government spending and budget outcomes.

Housing turnover can have a number of indirect effects on household spending. For example, housing turnover is positively correlated with household retail spending, particularly on durable goods such as furniture, home appliances and electrical or electronic devices (Graph 8). Renovation activity is another channel through which housing turnover can indirectly correlation between housing price growth and turnover. One strand of literature posits that changes in housing turnover can lead changes in housing prices if buyers and sellers have incomplete information about market conditions (Wheaton 1990).12 Changes in housing prices can subsequently affect household consumption via the household wealth channel (Muellbauer and Murphy 1990). Housing price growth can also affect dwelling investment by altering the expected return on investment, with flow-on effects for incomes and employment in related industries.

Changes in the composition of housing turnover, in particular the increase in the share of off-the-plan apartment sales, can affect the relationship between turnover, housing loan approvals and credit. For a typical sale of an existing property financed by a mortgage, the time between the contract date and settlement date is relatively short (around six to eight weeks). As a housing loan approval usually occurs about five to six weeks before settlement, this implies a short lag between housing turnover (recorded at the contract date) and loan approval. Credit is then drawn down at settlement of the transaction. As discussed above, off-the-plan apartments are commonly purchased before construction meaning that the lag between the contract date and settlement date can be around two or three years. As such, the loan approval and drawdown of credit does not occur until well after the initial contract is agreed (see ‘Box A: Housing Market Turnover and Housing Finance’ for more details).

Furthermore, housing turnover has a more general effect on household balance sheets.

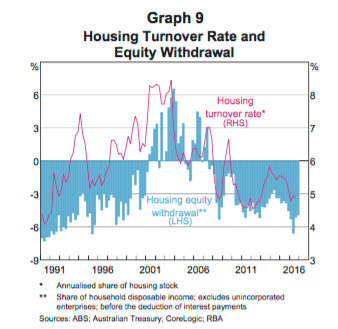

Higher rates of housing turnover have been associated with periods of housing equity withdrawal, which indicates an excess of mortgage borrowing over new investment in housing, and was seen in Australia for much of the early to mid 2000s (Graph 9) (RBA 2003). This relationship occurs because a housing transaction typically involves the buyer taking on more debt to finance the purchase than the seller has outstanding against the property (Schwartz et al 2006; Greenspan and Kennedy 2008; Reinold 2011). As a result, the current low level of the housing turnover rate might be expected to result in lower household leverage than otherwise.

Relatedly, lower rates of housing turnover will tend to increase the average age of housing loans and the level of mortgage buffers. Households with newer or larger mortgages have had less time to build up buffers, consistent with data from the HILDA Survey which show that borrowers with small or no buffers tend to be younger or have more recently taken out their loan (RBA 2012). Those households with large mortgage buffers tend to be older, suggesting they have had time to accumulate these.

Conclusion

The housing turnover rate has trended lower since the early 2000s. One contributing factor we highlight in this article is a lower propensity for households to move home. Among the potential reasons for this could be lower rates of home ownership, particularly for younger households, and migration trends.

More recently, the sharp increase in off-the-plan sales of new apartments, which are difficult to measure in a timely manner, suggests that reported housing turnover is likely to be understated. Given the significant settlement lags associated with these sales, the relationship between housing turnover and credit growth also appears to have weakened. Nevertheless, the longer-run decline in the rate of housing turnover suggests that housing-related activity could make a smaller direct contribution to aggregate economic activity in the future, and may also lead to lower household leverage and higher mortgage buffers.

Hannah Leal, Stephanie Parsons, Graham White and Andrew Zurawski work for the Reserve Bank.

Their article was published by the bank in the March Quarter 2017 update.

The Bulletin contains articles that discuss economic and financial developments as well as the bank's operations.

To view the release in full, go to the Reserve Bank website here.