RBA reaching the limits of its stimulatory solutions: CBA's Gareth Aird

GUEST OBSERVATION

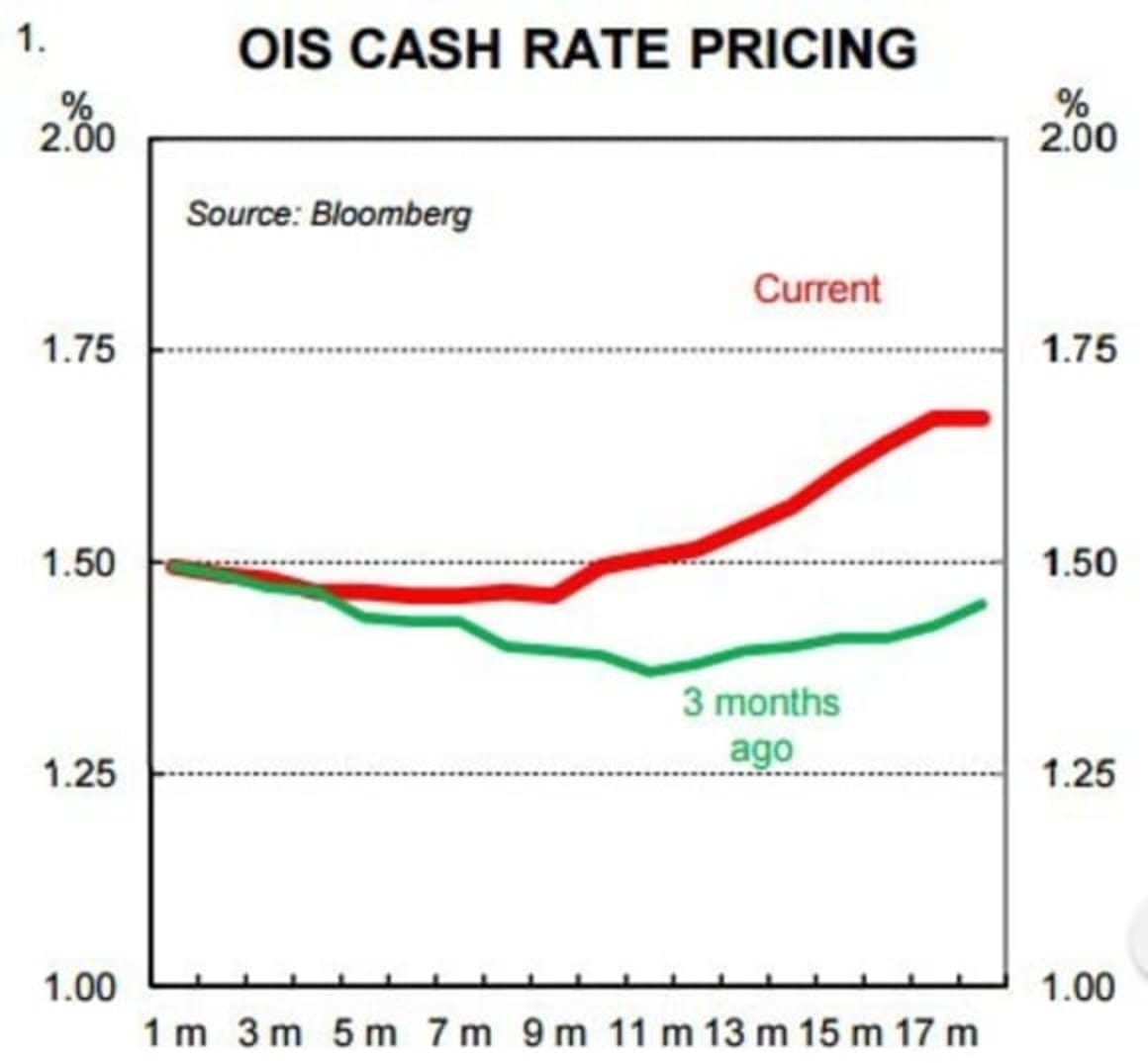

Over the past three months there has been a significant shift in market interest rates.

The yield curve has steepened and market pricing for another RBA rate cut has receded. Current market pricing indicates a small (15%) chance that policy is eased again. And it implies a 35% chance of a rate hike within the next 12 months.

CBA’s house view is that interest rates are on hold over 2017. And in our view, the risks over the year lie with a cut. But the steeping in the yield curve and shift in market expectations has led us to revisit our estimate of the neutral cash rate.

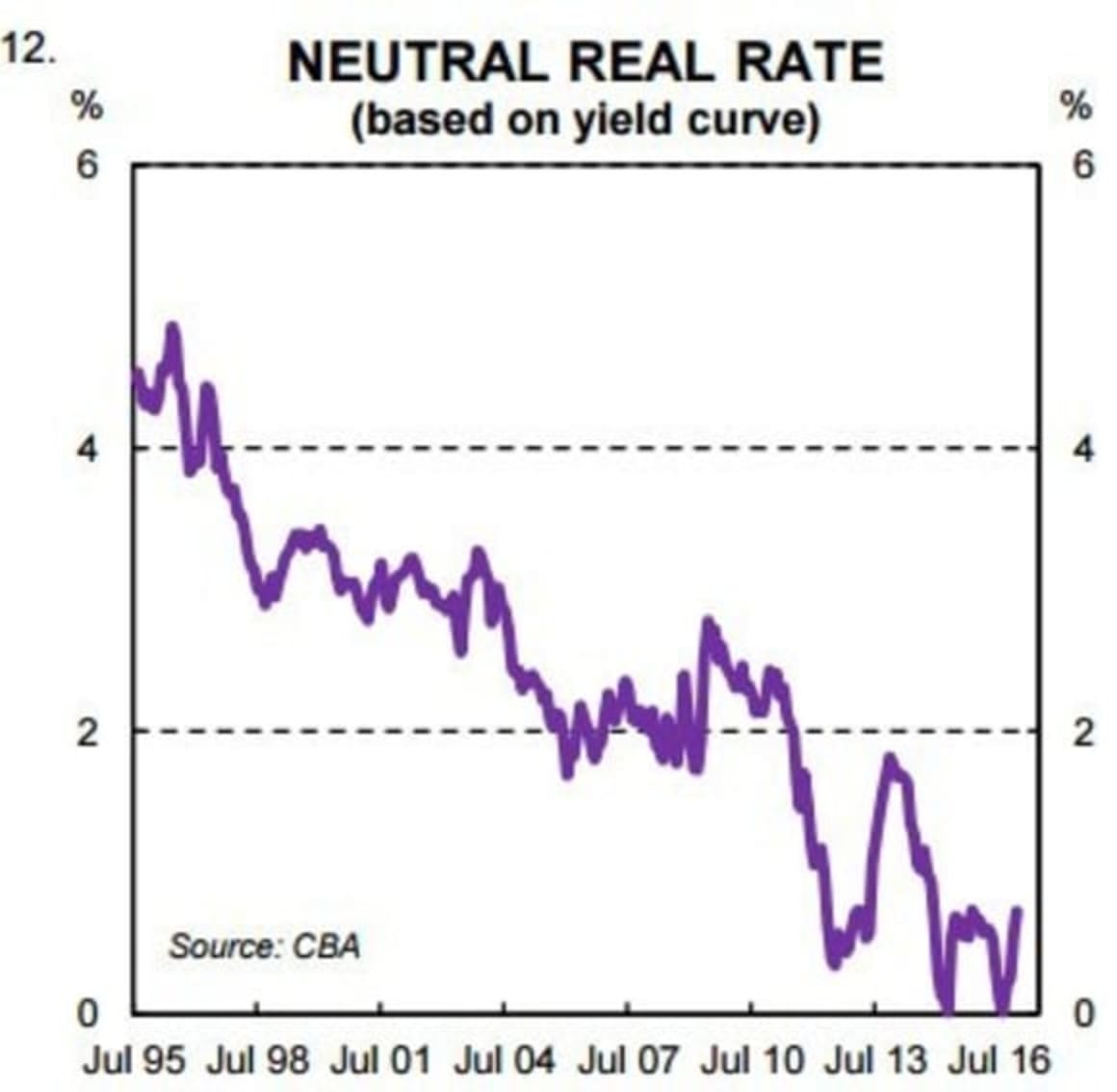

The analysis confirms our earlier work that neutral it is much lower than in previous cycles which means that the cash rate would not need to rise by much for policy to no longer be having a stimulatory impact on the economy. We estimate it to be 3% (2.5 – 3.5% range) which means that the current cash rate is about 150 bps in expansionary territory.

What is a neutral interest rate and why does it matter?

The level at which the RBA sets the cash rate can either have an expansionary, contractionary or neutral impact on economic activity. The neutral cash rate is the interest rate (or range of rates) consistent with full employment, trend growth and neither upward nor downward pressures applied on the price level through monetary policy. Or more generally, when the setting of interest rates is such as to exert neither contractionary nor expansionary forces on the economy, policy can be said to be ‘neutral’.

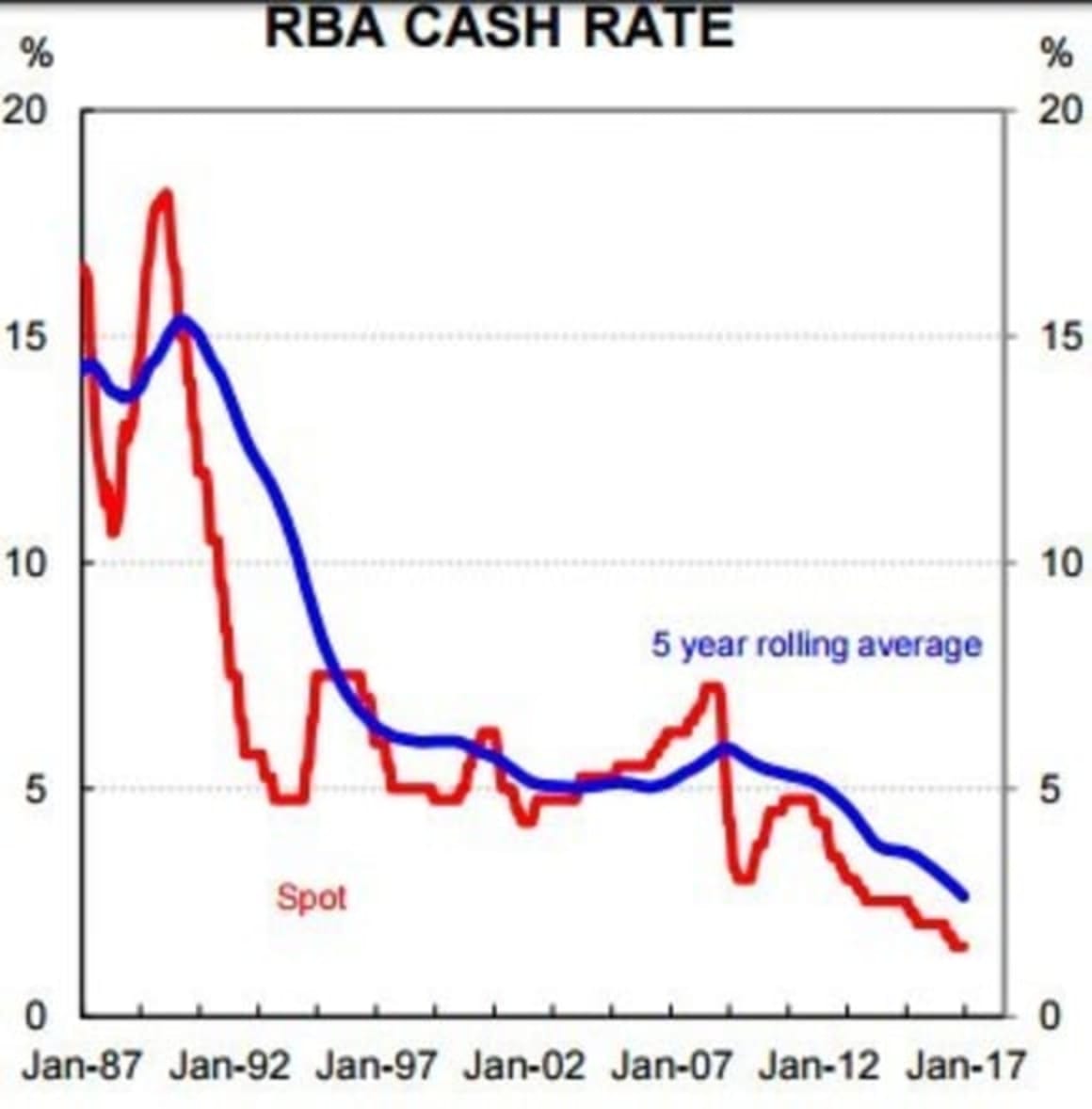

But the neutral rate it is not a constant rate. Rather it is influenced by changes in productivity, the stock of debt, lending margins, fiscal policy and the exchange rate. These drivers have moved in a way over the recent past that indicates the current neutral cash rate is probably at a record low.

The neutral rate is an important benchmark rate for evaluating the stance of monetary policy. It allows us to determine how expansionary or contractionary a particular policy setting is at any point in time.

One rule of thumb often used is comparing the level of the cash rate to a historic average cash rate to assess how accommodative or restrictive policy settings are. But that can be misleading because the neutral rate is fluid and varies over time.

When we compare current policy setting to the neutral rate they do not look as expansionary as implied by comparing the current cash rate to the historic cash rate average.

Policy implications

A range of estimates and theoretical arguments suggest that the neutral cash rate has moved to a record low. Our qualitative and quantitative analysis points to a neutral range of 2.5%-3.5% meaning a point estimate of 3%.

The analysis suggests that the RBA is faced with a relatively easy task if it needs to put the brakes on the economy at some point further down the road. It wouldn’t take a lot of tightening in policy to restore monetary policy to a neutral setting.

The flip side is that it becomes harder for the RBA to stimulate the economy as the neutral rate falls and we approach the lower bound. The limitations of monetary policy to stimulate growth become more apparent when the neutral rate falls towards the lower bound. The need for meaningful fiscal policy reform grows as a result.

We don’t see the RBA tightening over 2017. And in our view the risks like with further easing. Calls for fiscal policy reform in addition to higher levels of public investment will continue.

Gareth Aird is an economist at the Commonwealth Bank of Australia.

This is an edited extract of CBA Economics February 2016 report.