The impact of higher interest rates: Pete Wargent

There seems to be an awful lot of confusion about the role of interest rates in Australia, in particular from the house price crash cheerleading squad. On the one hand, they say that there will be a huge spike in unemployment in 2014, which will lead to a sharp property downturn - which may or may not be true. On the other hand, they say that higher interest rates will also return in 2014, resulting in the same impact.

Either one or the other of these statements might be true, but it's not likely to be both.

For the reasons I discussed here, the prospects for our economy are ultimately dependent on the strength of the labour force, and it seems unlikely that we will get higher interest rates until there is sustained evidence of an improvement in the employment data.ABS labour force figures are notoriously volatile month on month (variously due to relatively small samples, rotation of surveys and the non-response rate) and thus the Central Bank will want to see successive stronger releases before pulling the trigger on monetary policy tightening. A great start would be an increase in employment (+15,000 jobs) in Thursday's data for the month of September arresting the upward trend in the unemployment rate at 5.8%.

Source: ABS

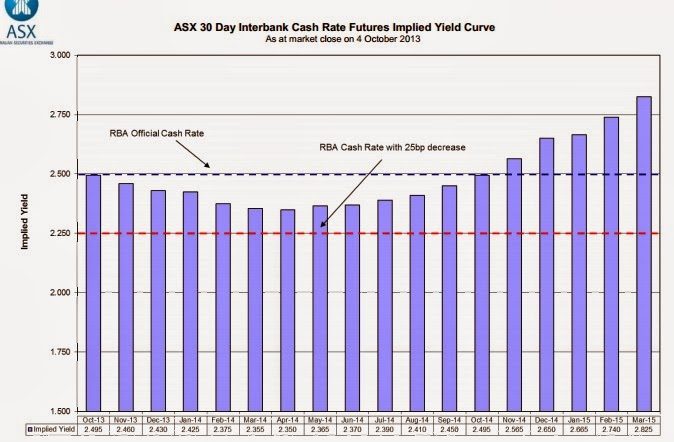

Unfortunately, with mining investment set to decline through 2014, at this stage, futures markets don't yet imply the Reserve Bank being in a position to implement an interest rate hike for quite some time to come yet - perhaps not even until early 2015.

Source: ASX

The impact of higher interest rates

Given the apparent level of confusion around, it might be worth having a quick re-cap of the likely impact of higher interest rates should they eventuate earlier than forecast.

Firstly, and perhaps most obviously, there would be higher variable rate monthly mortgage repayments for home buyers, mopping up more of their available household income and reducing the dollars which they have available to spend elsewhere.

Whatever anyone tries to argue 'in theory', the housing market is an interest rate sensitive sector and a hike (plus any associated expectations of mean reversion in the official cash rate) would almost certainly begin to apply some sort of a handbrake to speculative activity.As I see it, a hike in interest rates - and the associated expectation of further increases - would be likely to kill off material dwelling price growth in markets which have failed to build any momentum.

Everyone has their own opinion on dwelling prices. Mine is that a hike in interest rates could make for ongoing weak dwelling price performance in Hobart, Adelaide and certain regional markets. Canberra also faces challenges of a slightly different (although not unrelated) nature, which are tied back to a likely shrinking of its labour force.

On the other hand, a speculative beast has been unleashed in the Sydney housing market which may take more than a solitary interest rate hike to tame. In fact, based on what I've seen at auction, any market intervention at all is unlikely to stand in the way of the seemingly unstoppable momentum.

Note that as a Sydneysider I have a clear vested interest in this market, and therefore it makes far more sense to pay heed to what others forecast for our markets. That said, anyone who is based in Sydney will know exactly what I'm referring to - auction bidding frenzies, a proliferation of investors (with funds flowing from Sydney, inter-state and from overseas) and well-located properties in many cases selling for large margins above reserve.Secondly, higher interest rates would result in higher borrowing costs for industry. Correspondingly, higher interest rate charges will impact bottom line profits and potentially discourage companies from proceeding with marginal projects.

Similarly, other borrowing costs for individuals would increase for personal loans and credit cards, which eventually should impact consumer spending adversely (although the correlation may not immediately be as strong as it ought to be).

Due to lower corporate profits there may also be a fall in the value of ordinary shares, although the share market is clearly slightly more complex than that and momentum will as ever play a key role here too. In particular, value-orientated investors (as opposed to technical traders and speculators) are likely to weigh up the relative merits and yields of other available investments.

On the plus side, higher interest rates see stronger returns for savers and increase the returns that investors should typically expect to see on their money. This would be a relief for many pensioners who often prefer lower risk assets such as certain types of term deposit.What else?

Well, all other matters being equal, higher interest rates could see a return to the strengthening of our currency - the Aussie dollar - as overseas investors acquire assets to take advantage of higher returns. The price of bonds would also fall unless (a) the market and investors only see rising interest rates as temporary or (b) the interest rate rises have already been fully priced in.The most compelling reason why individual investors tend to look to property - apart from sticking to what they know - is the double-edged sword of greater available leverage.

Diverse economy

The blue collar press tends to report higher interest rates from the perspective of the individual homeowner: "Higher living costs." The white collar press often favours analysing the impact of interest rates on mortgage lending in general. Meanwhile, the business press tends to take a look at the broader impact of monetary policy and thus the impacts of interest rate decisions ripple throughout the pages of the paper in question.Interest rates are a blunt tool

Lest anyone need reminding, Australia is a massive and diverse country. London is significantly closer to Moscow than my place in Pyrmont is to Port Hedland. Up in the Pilbara iron ore exports are expanding at a rate that is - almost literally - unbelievable (up 46% year on year), resulting in an intense scrutiny of ongoing demand in China and the outlook for the commodity price. Yet elsewhere copper prices are languishing from the glory days of yesteryear and marginal projects have been shelved.

Of such a nature are the multi-faceted challenges facing the Reserve Bank. We have a manufacturing industry which has been slow, but a housing market in recovery. The RBA wants to stimulate dwelling construction yet keep a lid of speculative housing market activity. Business confidence has been shaky and the absolute level of mining investment looks likely to fade soon. And at this juncture, the unemployment rate still appears to be heading north. Let's hope that trend reverses soon.

Pete Wargent is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

His new book 'Four Green Houses and a Red Hotel' was released on 1 September 2013.