Inner city apartment supply past the peak: JLL

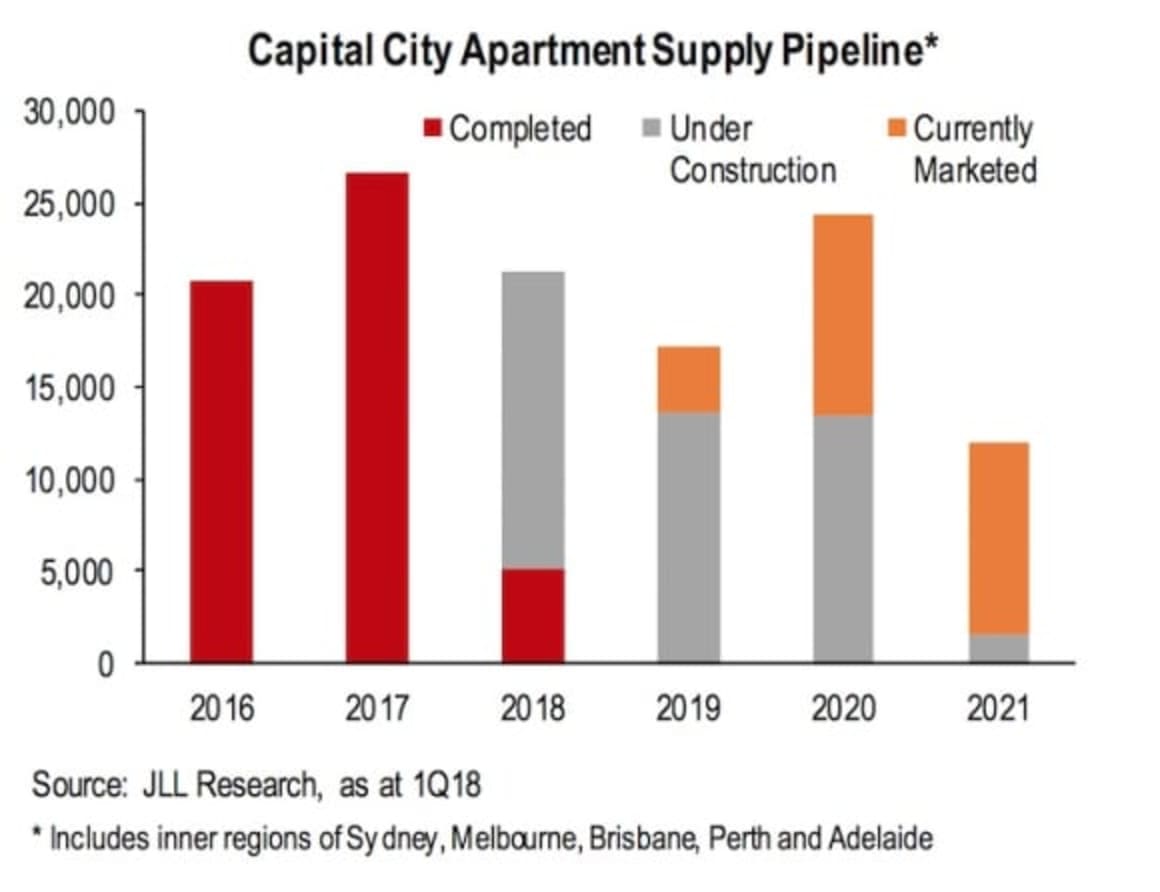

Nationally, current supply pipelines based on what is under construction and being marketed suggests supply will fall by around 20% over 2018 and by around the same amount again in 2019, according to JLL.

JLL’s latest Apartment Market reports for 1Q18 highlights that Australia’s major apartment markets are at very different stages of the cycle, but all markets are dealing with slower investor demand and tighter development lending conditions.

These factors have resulted in a thinning out of supply pipelines in all markets and means inner city apartment supply will fall in 2018 and 2019 from the highs of 2017.

JLL data suggests that around 26,600 new apartments completed in 2017 across inner city areas monitored in Sydney, Melbourne, Brisbane, Perth and Adelaide.

Click here to enlarge.

Current supply pipelines based on what is under construction and being marketed suggests supply will fall by around 20% over 2018 and by around the same amount again in 2019.

Leigh Warner, JLL’s head of residential research in Australia, says ultimately the shift in development focus is a good thing.

“There is no doubt that with slower investor demand it is now a very challenging environment for developers to meet pre-sales hurdles and progress the very large CBD and near-CBD projects that have typified this cycle," Warner said.

"Many of these projects have already been postponed to later cycles, abandoned, changed to alternative uses, or substantially redesigned to be a more manageable size in the current market.”

Nevertheless, development is not stopping and JLL’s reports highlights that the focus of developers in most markets has shifted from high-density to more medium-density projects, often in suburban infill locations and with high quality finishes to target the owner-occupier market.

“The decline in the inner city supply pipeline will be a much needed breather for most of our major markets and help them absorb the strong level of supply added over the past few years. But at the same time, strong population growth and the need to densify our cities, mean that we do need to keep building apartments or else supply will fall behind demand once more and price pressures will continue to plague our major cities.”

JLL’s 1Q18 reports continue to show large differences in where pricing and fundamentals are across the market. Sydney and Melbourne continue to both record low rental vacancy in spite of recent strong supply levels, but Sydney has shown more evidence of slowing apartment price and rental growth over recent months.

“Sentiment has clearly softened in the Sydney market and the market appears to be stalling now. However, Melbourne keeps on chugging on and showing remarkable resilience to recent supply levels. There is some moderate pressure on re-sale values in and around the CBD where recent supply has been particularly strong, but overall Melbourne’s strong population growth appears to be still cushioning the market from wider downward pressure.”

The reports also highlight that the Brisbane’s market appears to be stabilising after the worst of the supply wave is over and prices start to flatten out after 12-18 months of decline. Perth prices continue to fall, but there is also increasing evidence that it has passed the worst. This is evident in a recent rise in inner city apartment approvals, particularly for luxury apartments aimed at the owner-occupier market, which shows developers are gaining more confidence to start preparing for the next cycle.

Adelaide and Canberra are slightly less progressed in the current cycle and prices are still growing solidly despite elevated development activity. Momentum has slowed slightly in both markets over recent months, but the short-term outlook remains solid.