Residential construction: will boom lead to bust? CBA's Kristina Clifton

Australia is experiencing a long-running residential construction upturn, beginning around mid-2012.

Residential construction tends to be very sensitive to interest rates.

So falling interest rates from late 2011, combined with strong population growth, increased foreign demand and pent up demand from underbuilding in previous years meant that a boom was inevitable.

This building boom came at a very beneficial time and helped to offset some of the negative effects from the decline in business investment as the mining construction boom wound down.

The leading indicators of building activity suggest that the current residential construction boom has peaked.

So in this note we take a look at how the economy has benefited from the latest construction cycle and how it’s likely to fair as activity slows.

A typical residential construction upturn has both direct and second-round benefits.

The direct benefits include the additional building activity as well as the jobs created to undertake the additional building work.

Second-round benefits include additional spending elsewhere in the economy as a result of this new construction employment.

For example, spending on furnishings and household appliances for use in the new dwellings.

And then the additional employment as a result of this spending.

In terms of the direct benefits, residential construction upturns since the late 1970’s have on average contributed 2.2 ppts to GDP (chart 1).

The latest cycle has added 1.6 ppts.

Upturns also contribute to jobs growth. Employment in residential construction, has expanded by 38%, or by 31.2k jobs since 2012 (chart 2).

This is well above the 6.4% growth rate for total employment over the same time frame.

These jobs have been concentrated in NSW, Victoria and Queensland where the bulk of the residential construction has taken place (chart 3).

Other building construction jobs, which may include some workers employed in residential construction, have also expanded strongly over the latest residential construction upturn, with 38k extra jobs.

Jobs in construction services have also grown a little faster than total employment growth. Although this includes jobs related to all types of construction activity.

This expansion (and likely contraction) in residential construction jobs is much smaller than the rise in mining sector jobs during the mining boom.

We discuss this more in the next section.

The ABS has estimated that every $1m spent on residential construction generates 17 jobs on a full-time equivalent basis.

This includes jobs in the construction industry as well as the additional jobs outside the industry created as a result of flow on spending.

Spending on dwelling construction has risen by $6.2bn over the cycle so far.

So according to these multiplier effects approximately 105k jobs in total have been added to the economy.

The ABS has also estimated other second round benefits.

For instance, for every $1 spent on residential construction, $1.31 worth of spending is generated elsewhere in the economy.

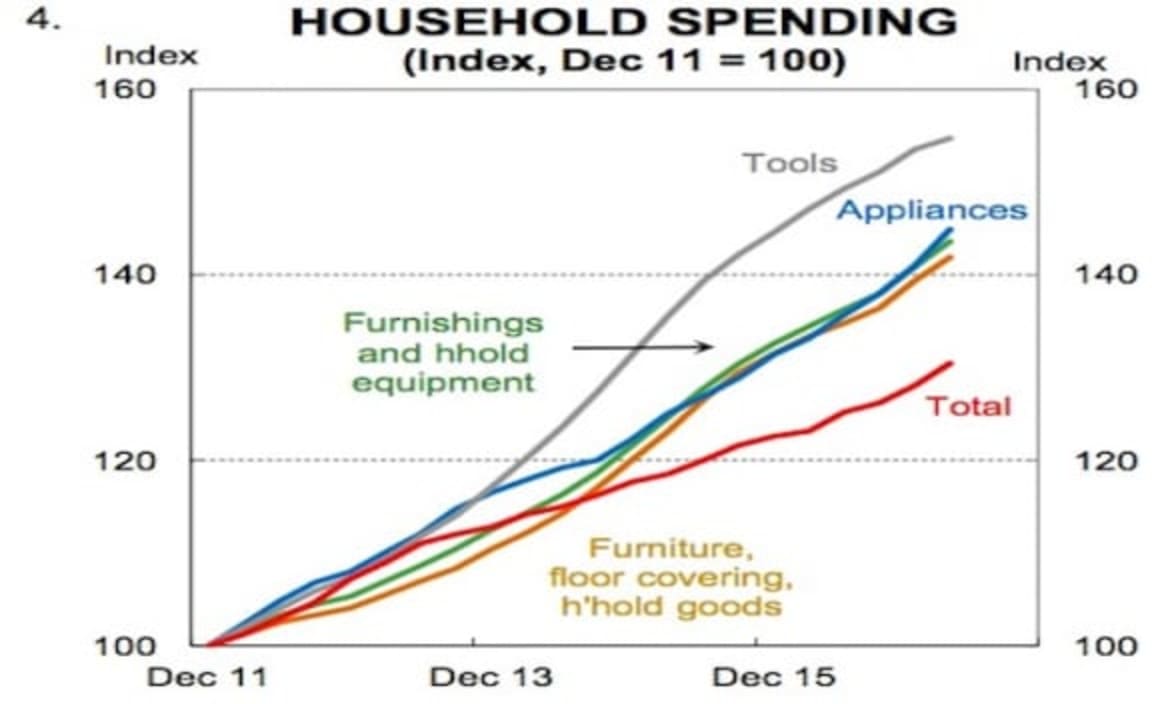

One area where we have seen this extra spending show up is in the category of household furnishing and fittings including household equipment, floor coverings, household appliances and tools.

Since the latest residential construction boom began, spending in these categories has lifted by 17.5% compared to 10.7% for total household consumption spending (chart 4).

This has been a positive for the retail sector which has faced many headwinds in recent years.

Other beneficiaries of residential construction booms are the State governments who collect stamp duty revenues.

The NSW, Victorian and Queensland State governments have all had solid growth in stamp duty revenues from the sale of residential properties.

Large house prices gains, particularly in Sydney and Melbourne, and decent turnover has also boosted stamp duty revenues.

In NSW, for example, stamp duty revenues have more than doubled over the past six years and now make up 32% of tax revenues compared to 22% in 2010/11.

We think the latest residential construction cycle has peaked. Residential building approvals peaked in August last year and have fallen by around 10% since then (chart 5).

However the pipeline of activity remains at record highs which means we are likely to see another quarter or two of growth in construction work done (chart 6).

We also saw a weather-related fall in residential construction activity in Q1.

This means that we are also due some payback in Q2.

However we think the downturn in the latest residential construction cycle will be gradual, and we expect an extended plateau where residential construction activity remains at a high level over 2017 and into 2018.

This is because a much larger share of approvals have been for multi-units than in previous booms (chart 7).

Multi-units have a much longer build time, averaging 6 quarters, compared to 2-3 quarters for detached houses.

Indeed some high rise apartments can take 2-3 years or more to build.

This prolongs the construction cycle.

On average, residential construction downturns have subtracted 1.5 ppts from growth.

Our forecasts running to the June quarter 2019 have dwelling construction subtracting just 0.5 ppts from growth.

The smaller subtraction from growth than average reflects the fact the upturn was a little smaller.

Also, strong population growth has lifted underlying housing demand.

We estimate that underlying demand now sits at 185k compared to 155k in mid-2012 at the start of the boom.

This means that the “normal” level of construction activity necessary to meet demand is higher than it was a start of the upturn.

We also expect renovation activity to pick up.

The fact that interest rate are likely to remain low for quite some time is also a factor behind our forecasts for a relatively shallow downturn.

We expect the RBA will leave the cash rate on hold until late 2018.

And that the tightening cycle from there on will be fairly cautious.

In terms of the number of dwelling commencements we expect a slowing to 200k in 2017/18 down from 217k in 2016/17.

And then a further decline to 185k in 2018/19.

For employment, we expect that job losses will occur fairly gradually alongside the gradual decline in activity.

This will help the labour market better absorb these workers.

There are a number of other reasons to expect that the disruption from the downturn in residential construction jobs to be minimal.

Firstly, the jobs downturn will be largest in NSW, Victoria and Queensland, the States where the lion’s share of building activity and gains in residential construction jobs have taken place.

These States all have decent population growth.

And two out of three of these States, NSW and Victoria have strong jobs markets. In NSW the unemployment rate is under 5%, and at a level consistent with full employment.

In Victoria, employment has been growing a solid pace and well above the national average.

Employment growth has also picked up in Queensland in recent months.

Secondly, both NSW and Victoria have also seen a lift in non-residential building approvals (chart 8).

So additional employment in the non-residential sector may provide a partial offset to some of the jobs losses in residential construction.

In fact the ABS estimates show that the multiplier effects from non-residential construction activity are even larger than for residential construction.

They estimate that $1m spent on non-residential construction generates 24 jobs on a full-time equivalent basis.

And for every $1 spent on non-residential construction, $1.47 worth of spending is generated elsewhere in the economy.

Thirdly, all three of these States have a large pipeline of infrastructure spending still to come from their respective State governments which should also add to jobs growth, especially construction.

The Federal government is also planning a large amount of infrastructure spending over the next 10 years which will also boost employment across the country.

Renovation activity should also provide an offset to lower new residential construction activity.

Renovations usually account for a little above 40% of residential construction activity.

However the share is now very low by historical standards (chart 9).

Current rates of spending on renovation activity also look low relative to house price growth (chart 10).

Strong house price growth usually encourages more spending on renovations.

There should be some catch up in renovation spending over the next few years.

Comparing to the recent ramp up and then decline in mining sector jobs, the decline in residential construction jobs will be much smaller.

Mining employment trended higher over a nine year period, rising from around 80k in 2003 to reach a peak of around 275k in mid-2012.

Since the peak of the mining boom around 50k jobs have been lost.

Although more jobs losses are likely as the construction of LNG facilities wind down.

These jobs losses have been concentrated in WA and Queensland. Queensland has had a construction boom and growing tourism sector to help offset lost mining jobs and activity.

But for WA there has been little in the way of other growth drivers to take the place of mining.

As a result economic conditions have been very soft for a number of years in WA.

In terms of the retail sector, a return to more normal growth rates for spending on household furnishings, furniture, appliances and other goods, would be another headwind for the retail sector to contend with.

Kristina Clifton is an economist with the Commonwealth Bank.