Sydney supply problems, investor finance through the roof and "ferry good" Neutral Bay

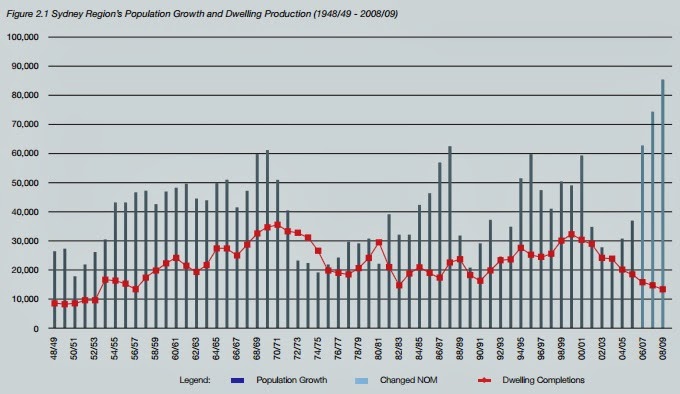

In 2009, Planning New South Wales released information highlighting its concern that dwelling completions were no longer tracking Sydney's exceptionally and increasingly strong rate of population growth.

Source: Planning NSW.

Planning NSW noted that over the 15 years preceding 2009, there had been three cycles of population growth and dwelling completions:

- In the first cycle, there was strong population growth and an equivalent upturn in dwelling completions;

- In the second cycle, both the pace of population growth and dwelling completions declined in concert; however

- In the third cycle from 2006 to beyond, it was noted that the rate of population growth boomed but dwelling production did not respond.

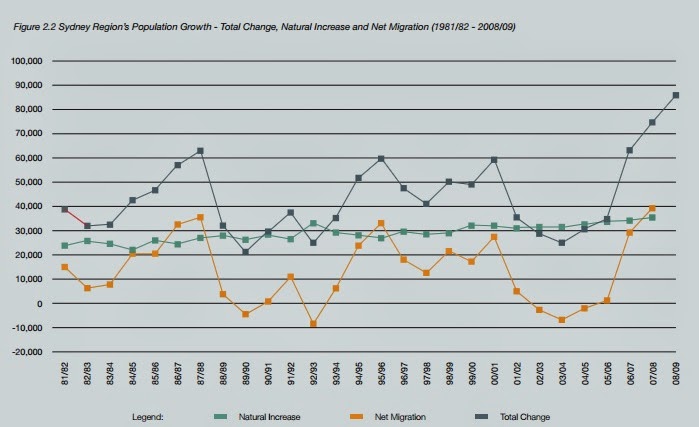

This upwards cycle in population growth was driven by a huge boost in net migration rather than a shift in the natural population increase, which remained relatively steady:

In FY 2006/7, Sydney's population increased by 63,000 with 29,000 of the increase accounted for by net migration. Yet by FY 2008/9 the increase in Sydney's population had jumped to a staggering 85,400, the change largely driven by an increase in net migration. This was not met with a meaningful dwelling supply response.

Source: Planning NSW

Population increase to continue for decades

The population of the Sydney region in 2009 was 4.5 million people which was 63% of the state’s population of 7.1 million. By 2036, pointed out Planning NSW, the Sydney region’s population was forecast to increase to 6 million which would increase its dominance of the State’s population to 66%.

With the number of lone person households and couples without children having increased, it was forecast that Sydney would need 770,000 new dwellings by 2036. In spite of this, dwelling completions were only tracking at depressed levels as charted above.

Demographics and approvals

Immigration was forecast to be heavily focused on inner- and middle ring suburbs.

Source: Planning NSW.

But in spite of the pressing need for new dwellings, approvals fell away.

Source: Planning NSW.

One of the main drivers for this was the unattractive return on investment for developers. Dwelling prices had done almost nothing since the 2003 boom and with net profit margins so slender there was little incentive to build, particularly since construction and development costs had also leaped dramatically over the preceding 15 years, the reasons for which I detailed here.

With median unit prices now having increased to around $550,000 in Sydney, there is a decent amount of dwelling construction underway, particularly of multi-unit dwellings.

Australia-wide construction is on track to hit 180,000 commencements in 2014, the second highest level of commencements ever reported, behind the 187,000 hit in 1984. But as evidence by the above chart, the margins are still too tight for developers to be particularly interested, and the situation balance remains fragile.

Today's construction may result in the risk of oversupply of overpriced new apartments in a few Sydney locations and hubs. I highlighted a few of the possible risk areas here, particularly in some of the new medium- to high-rise stock.

Article continues on next page. Please click below.

Supply issues to continue

However, dwelling commencements are forecast to tail off again in the coming two years while the population increase of New South Wales continues to stream into Sydney to the detriment of almost every regional centre in the state.

The major large cap developers - the companies with the resources and capital to resolve the supply issue - have shown very little interest in expanding their residential development plans dramatically, as can be seen on the respective company ASX releases. There is inadequate profit to be made to entice development.

Those working in the industry advise me that returns remain too low in the capital city residential development space, and thus the supply response is likely to dry up as soon as we encounter the next property price downturn.

Supply to fail to meet demand?

Reported the HIA yesterday, Australia needs to average 180,000 dwelling commencements per annum over the next 20 years in order to house its increasing population, but over the last 20 years we have averaged only 155,000 per annum:

"This 180,000 is simply not achievable under the current structural barriers to new housing supply".

The HIA cites disproportionately high taxes levied on the housing sector as a principal factor.

Other sources?

Other research houses have carried out research into the same topic and come to similar conclusion. This includes ID, and you can download their eBook on the supply subject here.

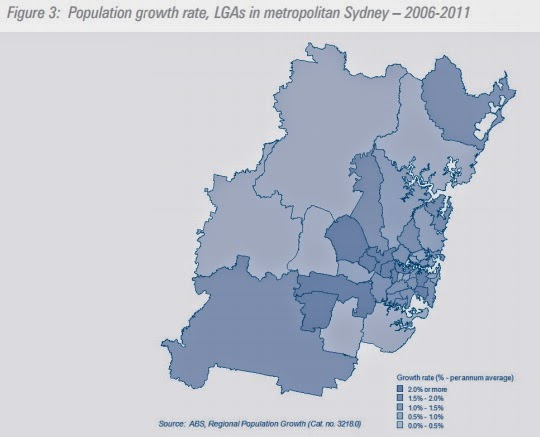

ID also found that population growth would be focused in Sydney's inner suburbs, with huge pressure on the inner west in particular:

Source: ABS, Regional Population Growth (Cat no. 32180)

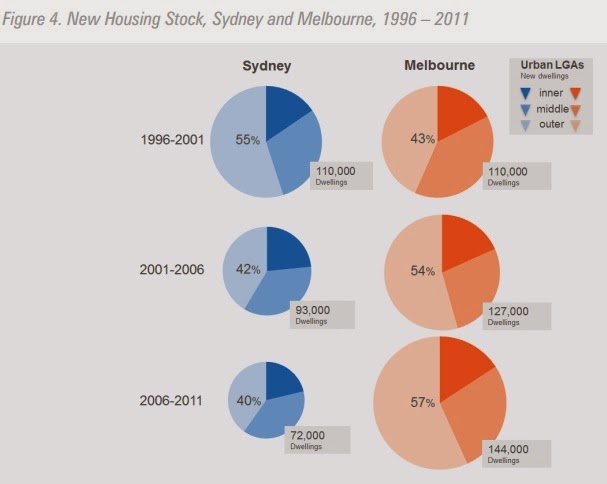

One of ID's interesting conclusions was that Melbourne has not struggled to bring supply online, the Victorian capital completing many thousands more units. Melbourne's problem has largely rather been one of bringing the type of supply online that people actually want to live in.

In both Melbourne and Sydney, only a minority of the new dwellings between 1996 and 2011 were located in inner suburbs.

Source: ABS, Regional Population Growth (Cat no. 32180)

I don't know as much about Melbourne as I do Sydney, but I do know that in the New South Wales harbour city most people want to live near the beach and the city. And, unlike Melbourne, Sydney just stopped building after its 2003 boom peaked leading to an utterly woeful supply situation unfolding and inevitably putting massive pressure on the market.

Source: ABS, Regional Population Growth (Cat no. 32180)

Summary

Since all of the above information has been publicly available and I chart it regularly, it was not difficult to predict that there would be no long drawn out property correction in Sydney in 2007/2008, since there was very little adequate supply and the population/demand was easily outstripping it.

It also wasn't hard to predict that eventually prices in the most popular inner west suburbs would inevitably boom, if you were following the data in any way. That horse has now well and truly bolted with apartment prices jumping by 56% in only five years.

On the other hand, with plenty of supply and lower demand, it was also evident that affordable options would remain in outer ring and fringe areas, and indeed they still do: to the north-west, to the west and to the south-west.

There are also very affordable housing options to the north and south of Sydney. However, the respective transport connections to these locations are poor, and need to be addressed as a matter of urgency.

The fact of the matter is that a large part of Sydney's supply problems revolve around far too many people wanting to live in far too small an area close to the city, and since that doesn't appear likely to change, inner city prices appear likely continue to rise over time.

Article continues on next page. Please click below.

Last week's ABS Lending Finance data showed owner occupier lending increasing by a seasonally adjusted 1.4% to $16,911 million in April.

And, as noted here too many times already, with the lowest borrowing rates we've seen in decades, investor lending appears likely to simply keep on increasing and pushing up the price of certain well-located dwelling types until either (a) interest rates are normalised (which is looking light years away at this juncture) or more stringent macro-prudential tools are deployed, whenever that may be.

Unsurprisingly, investor finance is now trending up across every state, but it is worth making the point once again that the flow of funds will be disproportionately skewed towards Sydney.

The impact of investor loans is likely to be minimal in low-demand regional areas and states where property investment is not considered to be popular.

Hot in Sydney...

By way statistical evidence, New South Wales investor loans increased in value on a rolling 12 monthly basis to yet another all-time record high of $46,346,211,000 - that is, $46,346 million.

In other words, investor activity is comfortably now sitting at a record high level which will drive the prices of certain property types in favourably located suburbs close to the city higher:

An unprecedented 46.8% of loans in New South Wales was for investment purposes in the month of April, implying in turn that more than half of loan values in the capital city of Sydney are likely to be accounted for by investors.

In other words, as we've long predicted, Sydney is now a maturing property market where prices will become exceptionally expensive in the inner- and middle ring suburbs as investors squabble over a limited volume of existing stock, and home ownership levels in those locations will ultimately recede.

But much cooler elsewhere...

By way of contrast, note what is happening (or more accurately, note what has not been happening) to investor loans in South Australia.

Despite the lowest interest rates in a generation, the rolling annual value of investment lending is below where it was in 2007, helping to explain why capital growth in Adelaide has been comparatively very poor.

There is very soft demand evident from investors, jobs growth is negative and has been for some years, and the state's population growth is weak.

A hotspot, 'tis not:

Steady as she goes...

Well, it was a so-so jobs report from the Australian Bureau of Statistics, the headline figures showing a decline of 27,000 part-time jobs, but an increase of 22,000 full-time jobs, leaving the total employed at a fairly steady seasonally adjusted 11,564,600:

In fact, the biggest plus I took away from this release is that the jobs growth in 2014 to date has been all about full-time jobs growth and not part-time positions.

Zooming in the chart a little shows that while the seasonally adjusted employment figures have been improving steadily when a meaningful amount of time is considered, the economy is still not yet adding jobs at the pace which would be desirable:

The unemployment rate has therefore held steady at 5.8% and it remains unclear whether the peak is yet in for the cycle or whether the headline rate of unemployment will head a little higher.

Probably the latter, and given that growth in the economy appears to be driven solely by net exports in the face of deteriorating terms of trade, it once again appears more than possible that the Reserve Bank's next adjustment to the official cash rate could be down to 2.25%:

Labour market by state

So, another year, another article imploring us to speculate in Adelaide real estate.

I've lost count how many years that is now, but probably, what, about the last six years or so?

One of the big trends which has unfolded across most of Australia over the past few decades has been the expansive growth of the two income household, which is one of the factors, in concert with falling interest rates, that has allowed dwelling prices to appreciate almost everywhere:

Sure, that's been all well and good for the years behind us, but what of the future?

One of the principal reasons I've had concerns about South Australia as a destination for property speculators over the years is that the underlying economy has remained weak, population growth is weak, and jobs growth has been all but non-existent.

If the local economy picks up, then fine I'll change my views accordingly, but it has to be said that the signals really don't look all that promising.

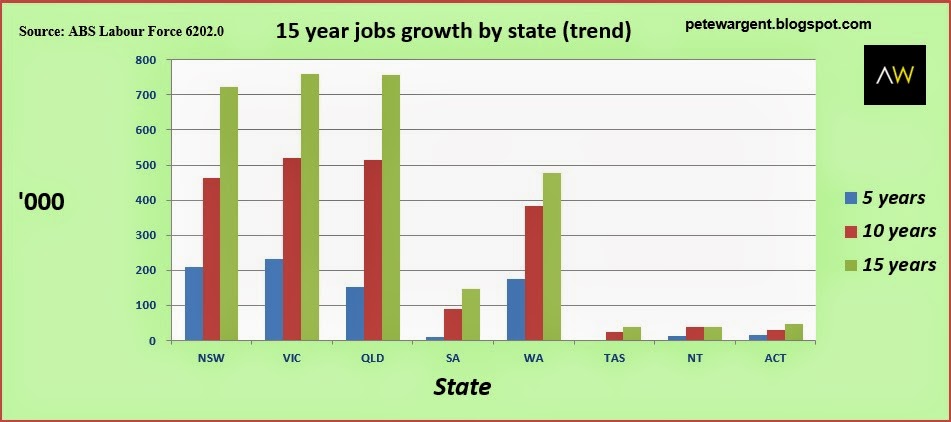

The total employment by state chart, not seasonally adjusted here hence the somewhat jagged appearance, reveals that only the four major states have been big drivers of jobs growth over the last 15 years or so:

The smaller states have struggled to add any jobs at all for fully half a decade now.

This important demographic trend is much clearer to see in a column chart.

South Australia has added only 11,000 jobs in five years, giving Tasmania - which has a net position of nil jobs added - a close run for its money as the worst economic performer:

Recent data was a good print for Victoria after some softer data in recent times, while Queensland has been the boss of jobs growth for the past 12 months (+60,700).

Meanwhile, South Australia produced another weak result and has shed nearly 20,000 positions in the same time period.

A minor point of concern, one would think, no?

DYOR, of course, and I'm just a bloke sitting behind a desk in Sydney CBD at Martin Place after all, but if that kind of employment print is apparently a signal to leverage up with abandon into Adelaide property, then I must be playing a different kind of game to the industry experts.

The unemployment rate by state shows an even more concerning picture for the southern states.

Elevated unemployment in South Australia (6.8%) and Tasmania (7.6%) is way too high for comfort - heck, even Great Britain has lower unemployment rates than that:

In fact, while the monthly figures are necessarily and forever volatile, the data reveals that only two states (Western Australia and New South Wales) have unemployment rates lower than the national average of 5.8%, and only one (New South Wales) which has been trending lower over recent times.

The main argument for buying property in Adelaide usually seems to revolve around the fact that it's cheap.

No arguments there, but with unemployment so high and trending higher, tens of thousands of jobs being shed and no available data to date implying a reversal, I'd suggest that you might only want to proceed with care and exercise a great deal of caution.

After all, cheap today is no use to anyone if it's cheaper tomorrow.

Article continues on next page. Please click below.

Ferry good

Was just over on the lower north shore, Sydney Ferries one of the more pleasant ways to experience public transport...it's also great to be able to use the Opal cards on Sydney Ferries now.

And Neutral Bay is one of the great suburbs.

The size of Neutral Bay is approximately 2 square kilometres and the suburb has four parks covering nearly 5% of total area.

The supply of new housing stock in these lower north shore garden suburbs is low, which puts continual upwards pressure on dwelling prices.

A little about the suburb...

Neutral Bay is a harbourside suburb on Sydney’s lower north shore.

The suburb is located approximately 5km to the north of the CBD in the local government area of North Sydney Council. Surrounding suburbs include North Sydney, Cammeray, Milsons Point and Cremorne.

Along the main road through the suburb, Military Road, is the main shopping district Neutral Bay Junction, It features many quality shops, restaurants and cafes. There is a shopping centre and mall with a supermarket and grocery shops.

The Oaks Hotel is a well-known and popular venue located on the corner of Military Road and Ben Boyd Road and has a number of restaurants and bars.

There are also quality schools nearby on the lower north shore.

Demographics

The population of Neutral Bay in 2006 was 10,213 people, yet by 2011 the population was 9,387 showing a population decline of 8% in the area during that time - and that's not due to increasing vacancy rates! There's essentially a very limited new supply of dwellings.

According to RP Data research, the predominant age group in Neutral Bay is 25-34 years.

Households in Neutral Bay are primarily childless couples and are likely to be repaying between over $4000 per month on mortgage repayments, and in general, people in Neutral Bay work in professional occupations.

In 2006, 44.6% of the homes in Neutral Bay were owner-occupied compared with 46.0% in 2011, representing a fairly steady result.

Currently the median sales price of houses in the area is around $1.4 million and units around $700,000.

In terms of income distribution, the greatest number of households sits in the $130,000 to $180,000 annualised income bracket.

Transport

The Neutral Bay ferry wharf is located at the end of Hayes Street and the Kurraba Wharf (see my photo above) on Kurraba Point can be accessed by Kurraba Road. Ferries run to the city with a travel time of around 10 minutes.

The Warringah Freeway runs along the western border of Neutral Bay, providing links south to the Sydney CBD and to the north. The road is often very busy during peak hours.

You can visit AllenWargent property buyers (London, Sydney) or Pete's blog.

His new book 'Four Green Houses and a Red Hotel' is out now.