Sydney out of top 10 leading prime residential markets: Knight Frank Wealth Report

The value of the world’s leading prime residential markets recorded slower growth in 2016, according to Knight Frank’s unique Prime International Residential Index (PIRI), which tracks the value of luxury homes in 100 key locations worldwide.

On average, values rose by 1.4 percent in 2016, compared with 1.8 percent in 2015.

However, the PIRI 100 also reveals a huge gap of 49 percentage points between the top and bottom ranking, up from 45 in 2015.

The top tier is dominated by cities in China, New Zealand, Canada and Australia, while oil-dependent markets such as Moscow and Lagos bring up the rear.

Of the locations tracked by PIRI, 61 percent recorded flat or rising prices in 2016, down from 66 percent the year before.

Along with the slight drop in average price growth already noted, this suggests a marginal slowdown in the performance of global luxury residential markets.

That said, there are several outstanding performers that will raise an eyebrow among even the most experienced investors.

China’s cities have catapulted themselves up our rankings with Shanghai, Beijing and Guangzhou claiming the top three slots, all exceeding 26 percent year-on-year growth.

Last year’s front-runner, Vancouver, was once again a top performer, but it was a year of two halves for Canada’s third most populous city.

Sales volumes grew ever higher leading up to the summer, before cooling off and then retreating after British Columbia imposed a 15 percent tax on foreign buyers in August.

Prime prices ended the year 15 percent higher, notably lower than the 25 percent increase recorded in 2015.

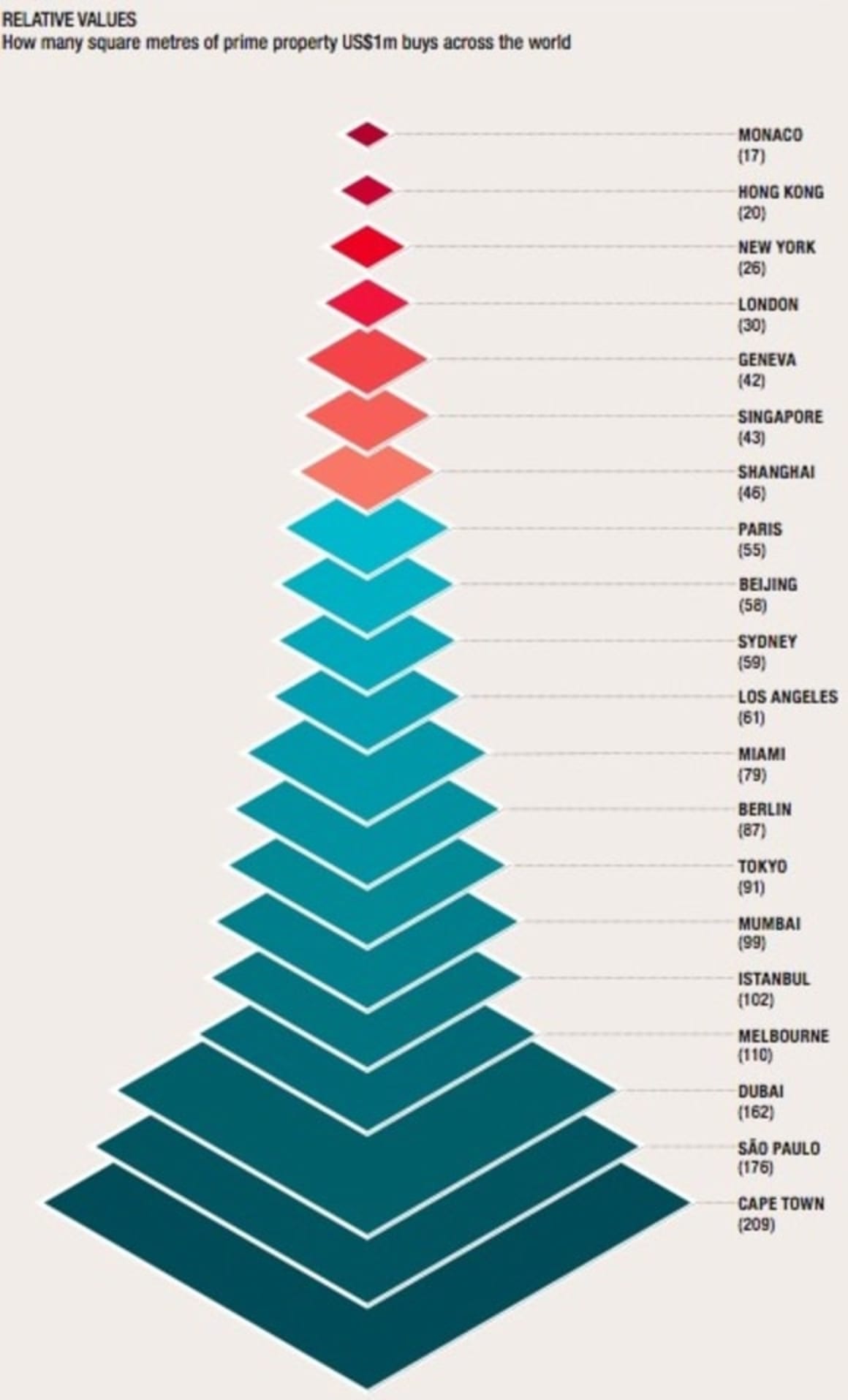

London, where many of the world’s super-rich have a home, slipped down the PIRI rankings with prime prices declining by 6.3 percent year-on-year.

The data shows it was the 3 percent hike in stamp duty for additional homes, introduced in April 2016, rather than the UK’s decision to leave the EU that helped to rein in demand.

But the tail end of 2016 saw an uptick in sales volumes and improved sentiment as the market readjusted to the new tax burden.

And what of the world’s other big-hitting financial hubs? New York had its challenges in 2016.

The strong US dollar negated some overseas interest and the delivery of a large number of new luxury projects helped inflate supply. But while volumes slowed, prices proved resilient.

With President Trump expected to embark on a programme of fiscal stimulus, reduced regulation and infrastructure investment, there is potential for stronger growth in 2017.

For its part, Hong Kong, which has languished in the bottom half of our PIRI rankings since 2014, has started to drift upwards, recording annual growth of 2.1 percent in 2016.

The increase would be higher were it not for the extension of a 15 percent rate of stamp duty that now brings Hong Kong residents (who previously paid 8.5 percent) in line with non-residents.

This latest tax change is just one of a raft of measures introduced since 2010 to keep a lid on price inflation in one of the world’s least affordable housing markets.

Given Hong Kong’s currency peg to the US dollar, some further relief may be proffered by the Federal Reserve if it restarts its rate-lifting campaign in 2017.

However, it will have to go some way to counter the demand from buyers based in mainland China, eager to hold a US dollar-linked asset.

Over the coming months, all eyes will be on policymakers in China as they attempt to reign in prices in the largest cities.

The wider mainstream market, where price growth of 30 percent year-on-year is not uncommon, continues to overshadow the luxury sector.

New cooling measures, including higher deposit rates and home purchase restrictions, have already been introduced in some cities in the hope of both slowing the rate of growth and deterring speculative demand.

By the final quarter of 2016, these were beginning to take effect.

While some of our strongest performers, such as Auckland, Sydney and Berlin, appear to have become permanent fixtures at the top of the rankings, a number of our newer prime movers, such as Guangzhou, Seattle and Amsterdam, can attribute their sudden ascent to the fact that their prime prices are rising from a low base.

Guangzhou, for example, now finds itself sitting alongside Shanghai in the rankings, having recorded 27 percent annual price growth.

Yet in real terms, prime prices here are half those found in China’s financial capital. Seattle and Amsterdam are also rising from a low base, but in both cases this can be considered a price correction following falls of 29 percent and 18 percent respectively post-Lehman.

Meanwhile, Europe continues to send out mixed messages. Of those locations recording a fall in prices in 2016, 50 percent were located in Europe.

A year earlier this figure was 65 percent, suggesting that the continent’s recovery is gaining traction. Amsterdam, Gstaad, Munich, Berlin and Barcelona were Europe’s top performers in 2016, but second home markets such as Ibiza, Mallorca, the Western Algarve and Lake Como also rose up the rankings.

A breakdown of the PIRI 100 by world region shows that Australasia (+11.4 percent), Asia (+5.1 percent) and North America (+4.5 percent) are the key engines of growth.

Europe and the Caribbean sit firmly “mid table”, recording moderate shifts of 0.5 percent and -0.3 percent respectively. Latin America (-2.7 percent), the Middle East (-3.3 percent), Africa (-3.4 percent) and Russia/CIS (-5.5 percent) all recorded negative growth, due to a combination of weak currencies, slowing economies, rising inflation, low oil prices and growing political risk.

Wealth creation and resulting cross-border flows have continued to shape prime property markets in 2016, with security concerns, currency movements, education and even healthcare also emerging as influential market drivers.

However, this year’s PIRI results highlight two key points.

First, local economic activity has a strong bearing on price performance (all of this year’s top 10 rankings report 3 percent or more in annual GDP growth).

And second, economic growth is firmly concentrated in the world’s cities (22 of the top 25 PIRI rankings are occupied by cities).

A breakdown of the PIRI results by property type also confirms this latter point.

Based on results from 2016, the value of a city-based luxury home increased by 2.4 percent on average, a ski home by comparison saw 1.9 percent growth, and a beach or coastal property slipped marginally by 0.5 percent.

The long-held “safe haven” narrative still has its place, but with strong capital growth eluding the world’s top financial capitals, we expect secondary markets across Europe and the US to come under the spotlight.

Cities that offer the potential for attractive margins, where prices are rising from a low base and where any risk is tempered by a level of transparency and good governance (Paris, Berlin, Madrid, Dublin, Chicago and Seattle) look likely to perform well.

Definition: UHNWI: Ultra-high-net-worth individual – someone with a net worth of over US$30m excluding their primary residence and HNWI: High-net-worth individual – someone with a net worth of over US$1m excluding their primary residence.