Years of structural shift to come for Australian economy: BIS Shrapnel

New South Wales is poised to lead the country in growth in the next two years, topping Victoria, even as the overall economy remains weak and the pain continues for the resources-powered economies of Queensland, NT and Western Australia.

According to the latest Economic Outlook bulletin by leading industry analyst BIS Shrapnel, the Australian economy will remain weak for some years yet until the non-mining sectors start to drive growth. However, the boost due to investment in housing will decline as as state-by-state housing peaks, and then falls, it adds.

"The structural shift has begun – albeit with years to come," says the report.

A lower dollar has boosted the key tradeables sectors: tourism, education services, agriculture, manufacturing industries and some business services, which power the economies of NSW and Victoria, the report says. The trade-exposed states of NSW, Victoria, South Australia and Tasmania, which had suffered under the high dollar from 2007 to 2014 – are now strengthening because of the increased competitiveness from the lower dollar.

“This is a major reversal in interstate relativities from just four years ago,” said BIS Shrapnel senior economist and report author, Richard Robinson.

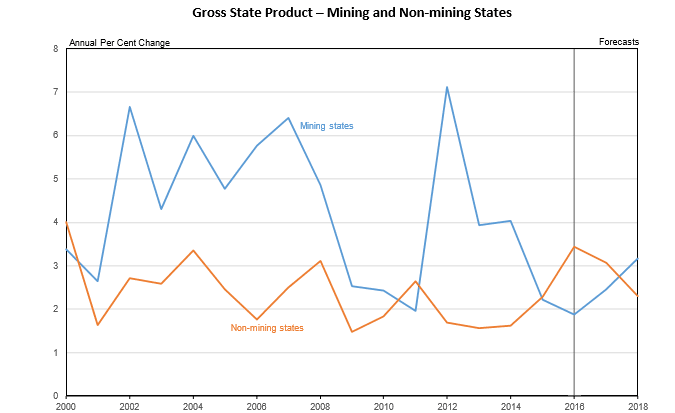

“For most of the decade to 2012, the mining investment boom saw Western Australia, Queensland and, more recently, the Northern Territory, record by far the strongest economic growth. Now, with the resources investment boom well into a substantial decline – and with more to come – they have been overtaken by NSW and Victoria. The pendulum is swinging away from the mining boom regions and states, and towards the states now being boosted by the lower dollar and their non-mining tradeables and services sectors.”

The peak in the mining boom and subsequent falls in both resources investment and commodity prices coincided with the 30 per cent decline in the Australian dollar (against the US dollar) to US72 cents in the March quarter 2016, although the dollar has since risen to US76 cents.

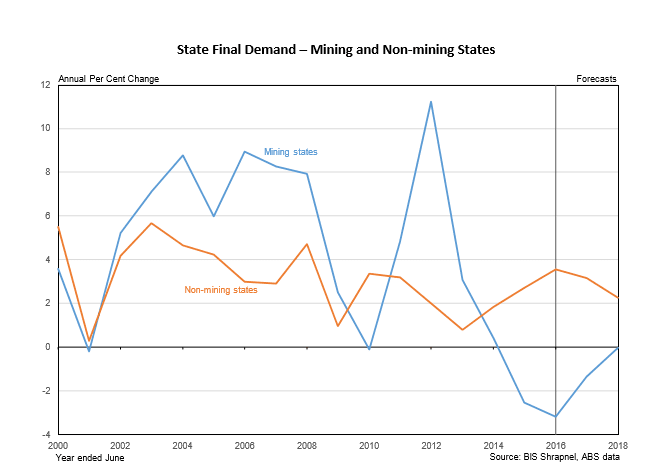

Among the states, there will continue to be marked differences in State Final Demand (SFD) according to the outlook for investment, which in turn will be a key influence on the prospects for employment and consumer spending in each state. Rising public investment in virtually all states will make a positive contribution to SFD growth.

This spending will also boost state output (Gross State Product) and employment, because public investment in infrastructure and buildings conveys significant multipliers through the economy via its high local content – except when governments don’t purchase local materials, such as steel.

"Dwellings investment also has high local multipliers, but the boost from this upswing is now set to diminish and then decline, as state-by-state housing peaks, and then falls. But it is the wide differences in the cycles of business investment which will have the most impact in determining state outcomes – particularly with regard to mining investment versus non-mining business investment."

These differences in investment and growth outcomes are a reflection of the structural change process which started with the upswing of the mining investment boom. This structural adjustment still has a few years before it finishes and the Australian economy returns to the balanced economy enjoyed before the mining boom.

“The temptation is to use the last decade’s growth as a benchmark against which to measure current progress. But the last decade was abnormal. It involved significant structural change as non-mining industries and investment ‘made room’ for the mining boom,” said Robinson. “We won’t simply see a uniform recovery over the next decade across industries and the states, back to the peak levels of the last decade. There will again be significant structural changes affecting the performances of industries and regions, this time away from mining and back to the non-mining industries that made room.

“That process will continue for some years yet. The norm isn’t a return to the averages of last decade, but a return to the pre-mining boom growth of the decade before. The Australian economy will remain weak for some years yet until non-mining sectors take over as the engine of growth.

“And while we navigate this structural change and major cyclical shifts, we’ll also have to cope with any fall-out from President-elect Donald Trump’s more outlandish policies – should his campaign rhetoric be translated into actual policies. But we’re optimistic that little of the more dangerous policies will be enacted, and that the world economy will continue to limp along.”