Property confidence dips as SME business conditions remain upbeat overall: Alan Oster

GUEST OBSERVER

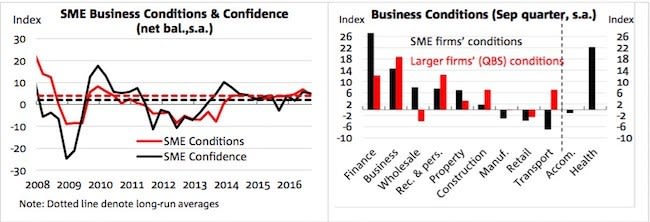

The Q3 NAB SME Survey suggests a loss of momentum in SME business conditions and confidence but this is against the exceptionally strong results in Q2.

Overall, conditions and confidence remain above their long-term averages which suggest relatively solid levels of underlying activity.

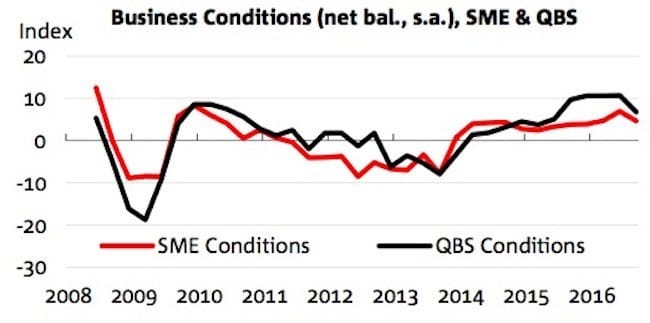

A further narrowing in the gap between conditions experienced by SMEs and larger businesses as indicated by the NAB Quarterly Business Survey suggests that the pace of growth is now more consistent across small and large businesses.

The NAB SME Survey is the leading business survey of small businesses in Australia, and complements the comprehensive Quarterly NAB Business Survey.

It offers a rich repertoire of insights into factors affecting smaller firms’ conditions by state, industry and size, as well as an assessment of their outlook for investment and output.

However, the base of industries which reported positive conditions shrank in the quarter and this warrants close monitoring for signs of further weakening in the near future. The sustained weakness in retail conditions is of particular concern as it has the potential to affect other affiliated industries such as wholesale and transport.

Meanwhile, we continue to witness strong conditions in tertiary services such as health, business and financial services.

SME business confidence eased marginally in the quarter to +5, but continues to exceed its long-term average of +2.

The fall in SME confidence was in spite of the RBA’s 25bps cut to the cash rate in August, perhaps a reflection of the absence of a sustained depreciation in the AUD despite the rate cut.

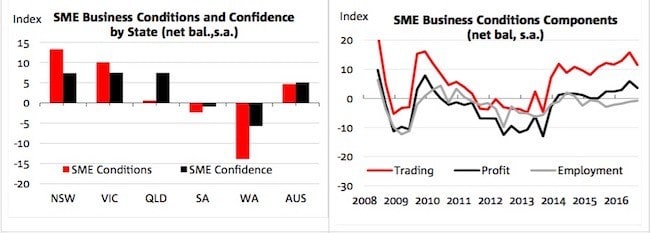

In Q3, business conditions were mixed by state. NSW, Victoria and WA reported relatively stable conditions, SA improved but was still lacklustre, while Queensland deteriorated sharply. The readings for Queensland in particular have been volatile recently so we will need additional information to determine the underlying trend for the state,” said Mr Oster.

NSW and Victoria continue to outperform in terms of conditions, while WA remains the weakest.

The ongoing mining downturn continues to weigh on WA conditions, while the recent improvements in commodity prices have done little to assuage the pessimism of SMEs from the state, with WA continuing to be the least confident state as well. Apart from WA, SA was the only other state to report negative confidence. Meanwhile, NSW, Victoria and Queensland tied in the top spot for confidence at +7 index points.

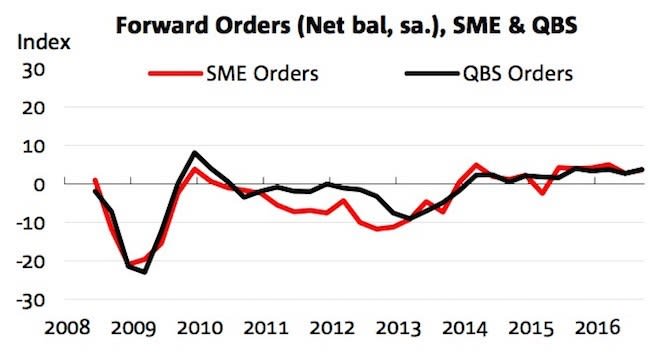

SME forward orders rose by 1 point to +4 index points in Q3, which is notably above the long-term average of -1 index points and consistent with the result for general businesses as reported in the QBS.

The generally positive readings for forward orders since late 2013 are broadly in line with a moderate recovery in real economic activity.

By industry, the quarterly movements were mixed. Apart from manufacturing, retail and transport, all other industries reported positive forward orders.

Forward orders for finance (up 16 points to +17) and health services (up 9 points to +16) jumped by the most in the quarter to record the strongest results, pointing to the continuing outperformance of services sectors.

Forward orders for manufacturing fell the most (down 8 points to -1). Meanwhile, transport and retail, both at -3, were the weakest in the quarter.

This is consistent with the lacklustre conditions and confidence experienced by the retail sector at the moment.

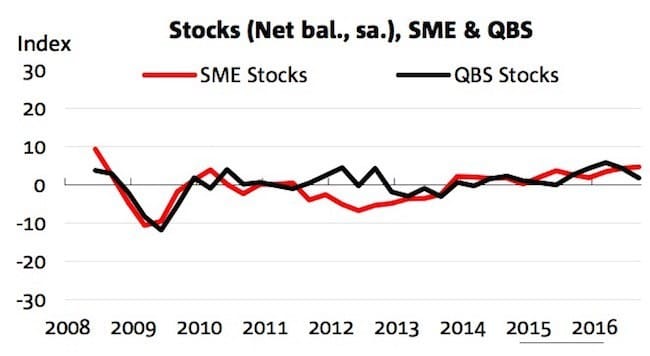

The SME stock index improved marginally to +5 index points, to be above the long-term average of +2 index points and that of larger businesses indicated by the QBS (at +2).

The improvement was largely driven by business services and health, both rising by 6 points to +13 and 0 respectively.

The stock index for business services was also the highest in the quarter, followed closely by wholesale (down 6 points to +11). The relatively high stock levels reported by the wholesale sector is consistent with a higher capacity utilisation rate and resilient forward orders in the quarter.

That said, the sharp deterioration in the conditions of larger wholesale businesses as indicated by the QBS could signal an imminent weakening of wholesale SMEs in coming quarters.

Meanwhile, stocks for manufacturing (down by 11 points to +3) and property services (down 9 points to -7) fell by the most in the quarter, with the latter the weakest across industries.

The two consecutive quarterly falls for property services are consistent with a lower transaction volume in the housing market recently.

The non-seasonally adjusted cash flow index was the strongest in Q3 for financial services (at +24), followed by business services (at +22) and the weakest for transport (-9) and retail (-8).

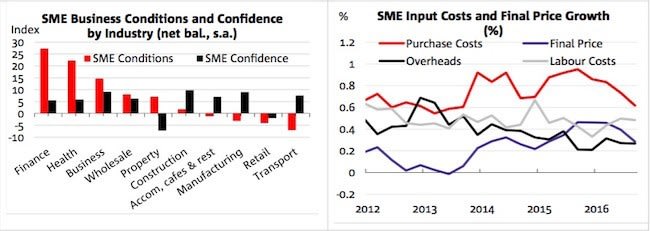

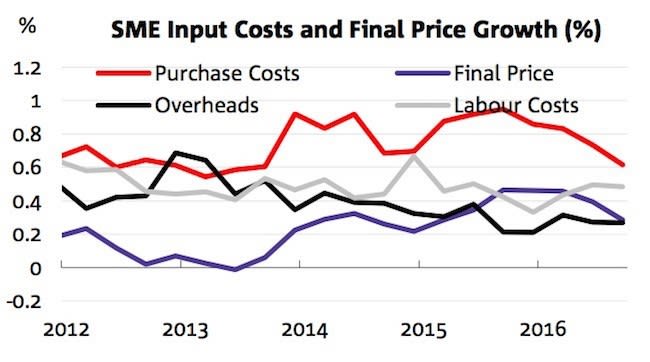

Overall, SME price indicators point to relatively contained price pressures.

Growth in input costs (purchase costs, overheads and labour costs) have generally eased over the last two years and have contributed to improved margins readings.

That said, final price growth appears to have lost some momentum in recent quarters – probably indicative of strong downstream competition – and is consistent with a subdued inflation outlook.

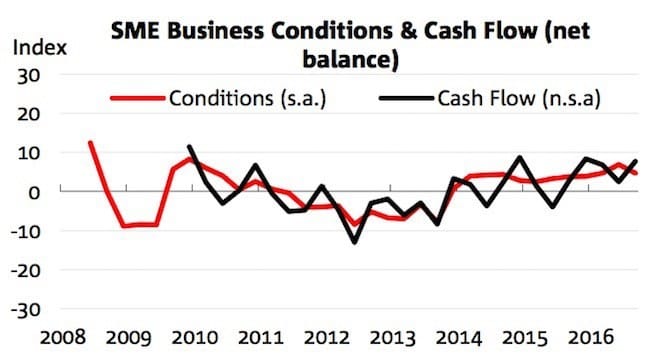

Business conditions for SMEs eased by 2 points to +5 index points in Q3, but remain slightly above the long-run average of +4.

Encouragingly, low-tier SMEs continued to report positive business conditions after recording the first positive reading in two years in Q2 to be around its long-term average.

SME conditions are now only marginally below those of general businesses indicated by the NAB Quarterly Business Survey (QBS), but this mostly reflects a notable fall in the conditions of the latter. SME business confidence also eased in the quarter to +5 (from +6 in Q2), but remains above the long-term average of +2.

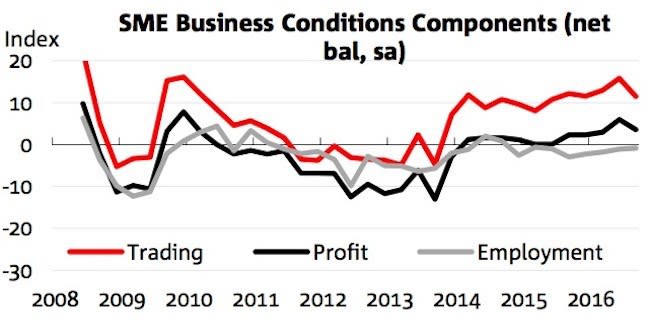

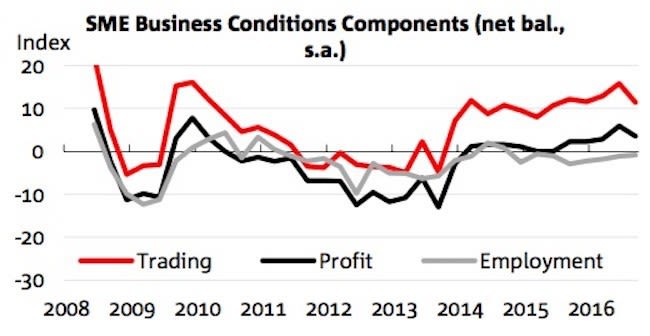

Two of the three components that make up SME business conditions fell, with trading conditions (down 5 points to +11) and profitability (down 2 points to +4) both retreating from their recent peaks but continuing to stay above their long-term averages.

Despite a sustained period where trading and profitability conditions exceed their historical average, the employment index was in negative territory for the eight consecutive quarter at -1, which was unchanged from the quarter before.

The lack of momentum in SME employment conditions are seemingly at odds with the relatively more robust reports by general businesses in the QBS, where the employment index has been tracking above long-term average levels since H2 of 2015.

This possibly reflects the weaker financial capacity of SMEs to hire new employees or a greater difficulty for them to find suitable labour compared to their larger counterparts.

In Q3, business conditions were mixed by state. NSW, Victoria and WA reported relatively stable conditions, SA improved but was still lacklustre, while Queensland deteriorated sharply. The business conditions index for Queensland gave up all its the gains, dropping by 10 points from Q2 to be back at +1 again.

The eastern non-mining states of NSW and Victoria continue to outperform at +13 and +10 respectively, while WA remains the weakest of all states at -14. Despite the sharp fall in conditions, Qld was the only state which reported improved confidence in the quarter (up 2 points to +7) to tie with NSW and Victoria in having the strongest confidence.

Meanwhile, stronger commodity prices in the quarter had done very little to bolster confidence of SMEs in WA, which reported a decline in confidence (down 5 points to - 6) in the quarter to be the weakest of all states.

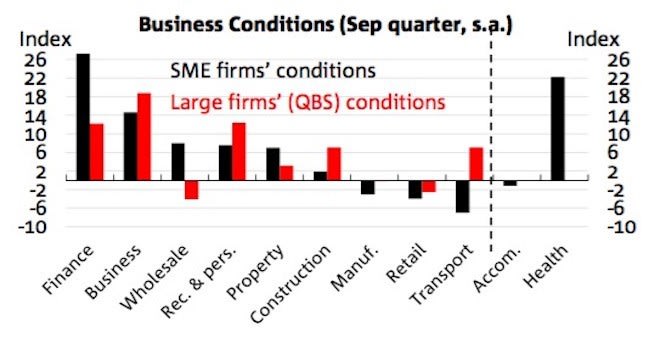

Most SME industry sectors reported weaker conditions in the quarter, with services sectors continuing to outperform more traditional sectors in general. Similar to Q2, health, finance and business services occupied the top three spots, while transport (at -7) replaced construction (at +2) as the weakest sector, followed by retail (at - 4).

The wholesale sector managed to hold onto its recent gains in conditions to be at +8 index points, a sign that perhaps some of the earlier upstream cost pressures had ameliorated. However, weak growth in wholesale final price suggests that competitive pressures downstream are elevated.

Business confidence by industry paints a more positive picture overall, with more sectors reporting an improvement rather than a decline in the quarter. Apart from property and retail, all other industries recorded positive confidence.

Somewhat surprisingly, confidence of the property sector suffered the sharpest decline in the quarter to be the weakest across industries, even though dwelling prices continue to grow strongly in major markets of Sydney and Melbourne, and more recently, ACT.

Compared to the larger businesses in the QBS, SME business conditions outperform general businesses in finance, wholesale and property, but are significantly weaker in transport.

Analysis by firm size shows that low-tier SME firms continue to report weaker conditions and confidence compared to their larger counterparts, although the fact that their conditions and confidence indices are positive remains encouraging.

Alan Oster is group chief economist, National Australia Bank, and can be contacted here.