Dwelling prices and the current state of play: HIA's Shane Garrett

GUEST OBSERVER

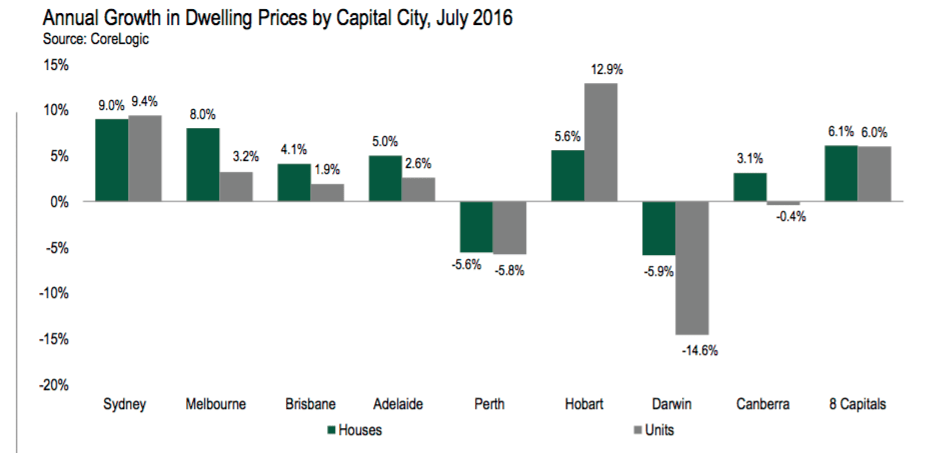

Across Australia’s capital cities, price growth has slowed with house prices up 6.1 percent in the year to July 2016 and unit prices increasing by 6.0 percent.

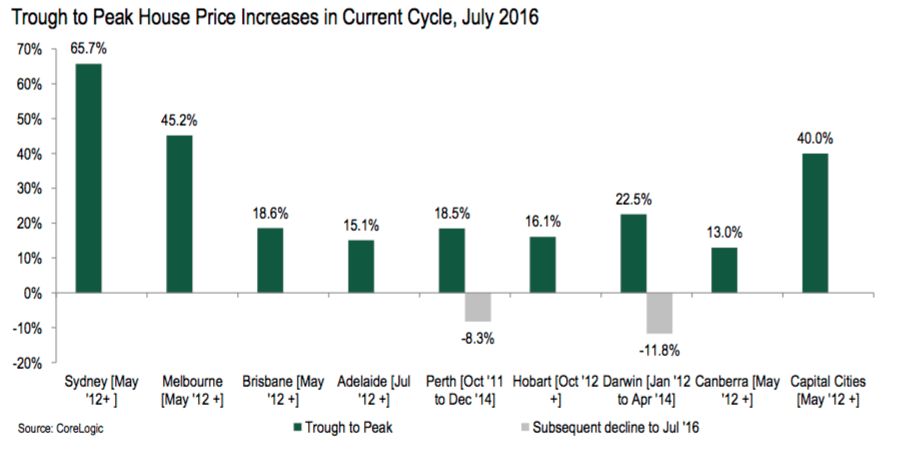

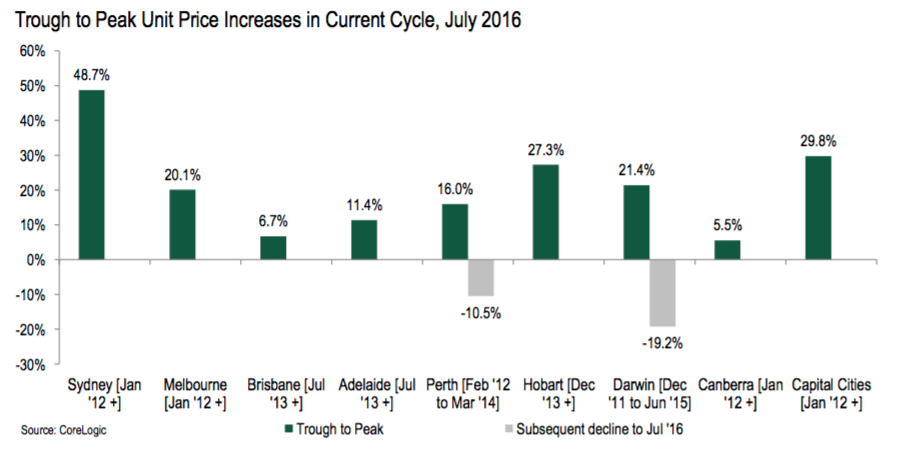

Since the low point in 2012, capital city house prices have increased by 40.0 percent in aggregate while unit prices rose by 29.8 percent. Unit prices started to recover a few months earlier than house prices;

Since bottoming out, the divergence between dwelling price growth in the different capital cities has been remarkably wide. The biggest uplifts have been in Sydney (+61.3 per cent) and Melbourne (+42.0 per cent). At the other end of the scale, Perth (-8.3 per cent) and Darwin (-12.7 per cent) prices have fallen substantially since peaking in 2014;

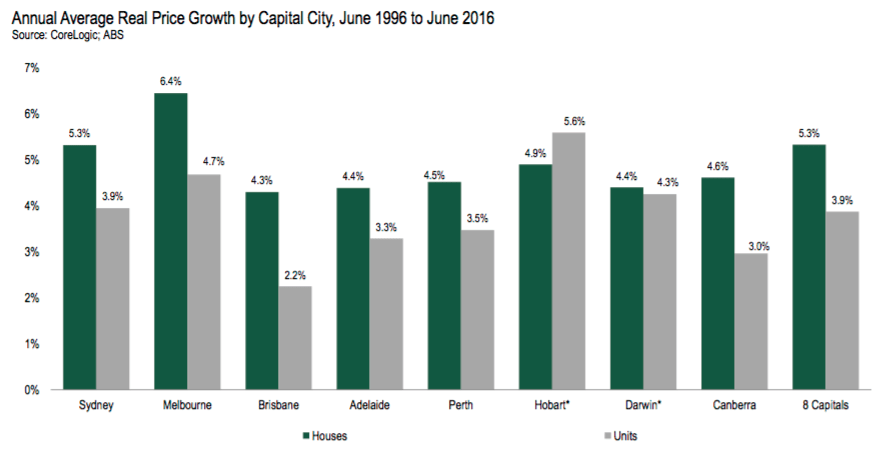

Despite the considerable variation during the current cycle, price growth across the capital cities has been quite uniform over the past two decades. In real terms, house prices have increased by 5.3 per cent annually compared with 3.9 per cent growth in unit prices;

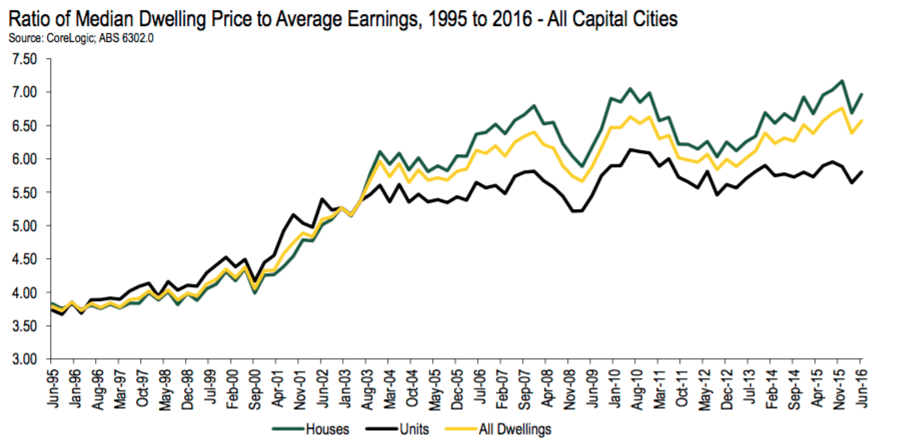

The ratio of the median dwelling price to average earnings has increased substantially over the past two decades. Much of this is explained by structural changes in household size, economic participation rates, earnings patterns and the level of mortgage interest rates;

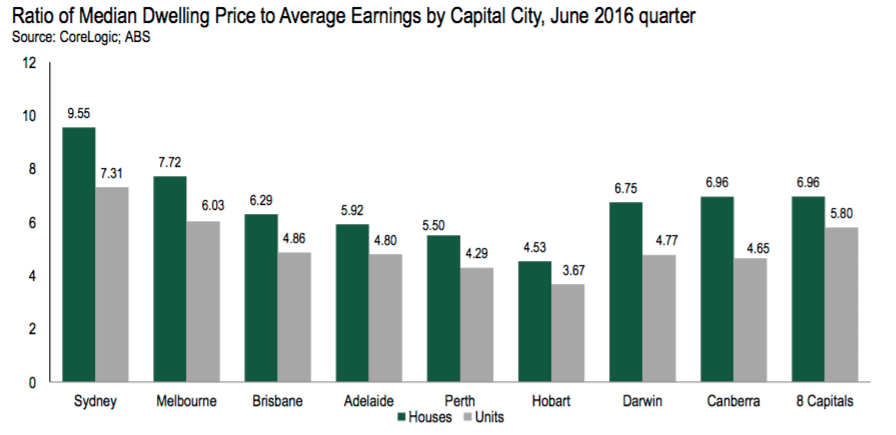

During the June 2016 quarter, the price to earnings ratio was 6.96 for houses and 5.80 for units. The highest ratios were in Sydney and Melbourne, with the lowest in Hobart and Perth. With the exception of Sydney, affordability is more favourable than the 15-year average in all capitals;

With respect to wider economic and financial conditions, dwelling prices across Australia appear to be proportionate. However, the wide geographical variation in current conditions means than some markets are likely to experience significantly stronger price growth than others over the medium term.

This is an update of the HIA Economics note on dwelling prices which was released in November 2015.

That piece of research then reported on how annual dwelling price growth across Australia’s eight capital city markets reached 10.1 per cent during October 2015. Since then, the pace of dwelling price growth has slowed and latest data show that dwelling prices increased by 6.1 per cent during the year to July 2016. Over this period, detached house price growth (+6.1 per cent) was almost exactly the same as the growth in unit prices (+6.0 per cent). Later, we explore in greater detail the relationship between house price growth and unit price growth over time in each of the capital city markets.

As was the case late last year, the variation in dwelling price growth trends is very large when comparing capital cities. The chart below illustrates the changes in house and unit prices in each of the capital cities over the year to July 2016. House prices saw the largest increase in Sydney over the year (+9.0 per cent) followed by Melbourne (+8.0 per cent). Over the same period, the largest increase in unit prices occurred in Hobart (+12.9 per cent) and Sydney (+9.4 per cent). Despite the strong uplifts in several markets, house prices fell quite significantly in both Perth (-5.6 per cent) and Darwin (-5.9 per cent). Over the year, unit prices declined in three capital cities: Perth (-5.8 per cent), Darwin (-14.6 per cent) and Canberra (-0.4 per cent).

Aggregated data for the eight capital cities indicate that dwelling prices bottomed out during May 2012 and have since expanded fairly consistently in all capitals apart from Perth and Darwin. The chart below summarises the cumulative increase in detached house prices in each market during the current cycle. Overall, detached house prices increased by 40.0 per cent across the eight capitals between May 2012 and July 2016. The largest house price rise occurred in Sydney over this period (+65.7 per cent), followed by Melbourne (+45.2 per cent) and Brisbane (+18.6 per cent). In contrast, house prices in Perth and Darwin have fallen back since reaching their peaks in 2014. Perth house prices have declined by 8.3 per cent while Darwin house prices are down by 11.8 per cent. Of the cities that have experienced consistent price growth, Canberra has seen the smallest increase in house prices since the 2012 trough (+13.0 per cent).

The comparison between prices for detached houses and units in terms of growth is illuminating in several respects. The increase in unit prices has been significantly less pronounced during the current cycle. Also, the upturn in unit prices appears to have commenced about six months earlier than the recovery in detached house prices. Whereas detached house prices have increased by 40.0 per cent during the current cycle, unit price growth has been about 10 percentage points lower (+29.8 per cent). Over the same period, detached house prices have outpaced unit price growth in every single capital city apart from Hobart. This may be related to the smaller sample size in Hobart, as well as the shorter timeframe being analysed for the city.

The pace at which detached house prices have outrun unit prices during the current cycle is greatest in Brisbane (18.6 per cent v 6.7 per cent), followed by Canberra (13.0 per cent v 5.5 per cent) and Melbourne (45.2 per cent v 20.1 per cent). It is also worth noting that in the Perth and Darwin markets where prices are falling, unit prices have dropped considerably faster than detached house prices. Hobart is the only capital city where unit prices have increased by more than detached house prices in the current cycle (+27.3 per cent v +16.1 per cent). The behaviour of prices in the current cycle underlines the great degree of heterogeneity both across and within the capital city markets.

How do dwelling prices behave over the long run?

Assessing dwelling price growth over time allows us to net out the effects of cycles and temporary factors and capture a sense of long-term trajectory of price dynamics. The chart below illustrates the real annual average growth rate for both detached house and unit prices over the 20-year period to the June 2016 quarter (due to data availability constraints, a 15-year timescale is used for both Hobart and Darwin). These data suggest that growth in real detached house prices tends to outpace unit price growth over the long run (5.3 per cent v 3.9 per cent per year). This was the case in each of the eight capital cities, with the single exception of Hobart.

Perhaps the most striking takeaway is that real dwelling price growth rates across each of the eight capital cities tend to lie within a relatively narrow band over the long run, especially in the detached house market. Real detached house price growth was strongest in Melbourne over the two decades in question (+6.4 per cent annually) and weakest in Brisbane (+4.3 per cent) over the same period. However, six of the eight capital cities were all less than one percentage point apart in terms of real detached house price growth on an annual basis (ranging from 4.4 per cent to 5.3 per cent per year).

Compared with detached house prices, the divergence in real unit price growth has been wider from city to city. Over the long term, Hobart units have experienced the largest increase in real terms (+5.6 per cent annually) with the slowest pace of growth in Brisbane (+2.2 per cent per year). In the other six capitals, real unit price growth has been concentrated in a relatively narrow range of between 3.0 per cent and 4.7 per cent annually.

Despite the considerable differences in economic structure, geographies and the regulatory framework across Australia’s eight capital cities, real dwelling prices still behave in remarkably similar ways from city to city over long periods of time with detached house prices consistently growing more strongly than those of units, although there tends to be much greater price variation on the unit side of the market.

A possible implication of this is that those markets which have seen recent the strongest price growth exceed the long term average in the recent past are most at risk of below par price performance over the coming years. By the same token, the markets that have recently seen price growth underperformed the long term average rate performed weakest in terms of price are most likely to see future acceleration in price growth.

Price to Earnings: the relative price of housing

While median disposable household income is the most conceptually sound indicator for benchmarking dwelling prices relative to income in the economy, the fact that these data are released only once per year with a long lag means that other measures must be utilised for more timely and frequent updates. Accordingly, this note uses average earnings as a barometer for household income due to the fact that earnings data are produced twice yearly (for the May and November ‘quarters’) in a relatively timely fashion. However, it is important to note that earnings data are an imperfect gauge of households’ financial resources, as no account is taken of direct taxation, unearned income (such as pensions, etc.) and income in kind.1

Based on the average earnings data available from the ABS, the chart below provides an overview of the median dwelling price to earnings ratio across Australia since 1995, including data for detached houses and units. Over this period, the ratio has increased from 3.79 in the June 1995 quarter to 6.57 during the June 2016 quarter. The median detached house price is now 6.96 times earnings, compared with 3.83 in June 1995. On the unit side of the market, the price to earnings ratio has increased from 3.73 to 5.80.

At first glance, this suggests that dwelling prices have lost touch with prices and incomes in the economy. However, the big uplift in the price to earnings ratio can largely be explained by two structural changes over the past 20 years. First, the number of employees per household has risen significantly over the two decades due to higher female labour force participation rates, a trend towards taking retirement at older ages and changes in the structure of some households involving greater numbers of young professionals in ‘share’ housing. The secular reduction in interest rates over this period has also permitted dwelling prices to grow faster, due to the fact that homebuyers can affordably service much larger mortgages at current interest rates than was the case when the interest burden was much higher. It is worth noting that the RBA’s Official Cash Rate in August 2016 of 1.50 per cent is only one quarter of the 6.00 rate in August 2006 and an even smaller fraction of the 7.00 per cent cash rate of August 1996.

Given the wide variation in dwelling price levels across Australia, it is useful to compare the ratio of dwelling price to earnings in the eight capital cities. This is shown in the chart below for each city during the June 2016 quarter for both detached houses and units. In Sydney, the detached house price to earnings ratio continues to be the highest in the country but eased back to 9.55 during the June 2016 quarter, after reaching an all-time high of 10.31 during the final quarter of last year. Detached house price to earnings ratios are also elevated in Melbourne (7.72) and Canberra (6.96). The ranking in terms of unit price to earnings ratios is similar: it is highest in Sydney (7.31), followed by Melbourne (6.03), although Brisbane is in third place (4.86).

The detached house price to earnings ratio is lowest in Hobart (4.53), followed by Perth (5.50) and Adelaide (5.92). In terms of unit prices, the pattern is similar. The price to earnings ratio is lowest in Hobart (3.67), followed by Perth (4.29) and Canberra (4.65). Across the eight capital cities, the detached house price to earnings ratio in the June 2016 quarter was 6.96 with the median unit price at 5.80 times average annual earnings. The tendency of dwelling price growth rates to converge implies that the capacity for future dwelling price growth is most limited in those markets where the ratio of dwelling prices to earnings is high, and vice versa.

The importance of affordability

While the dwelling price to earnings ratio is a useful snapshot of valuations, it does not take account of changes in financing costs which have fallen sharply over the past decade. The chart below provides an estimate of affordability in both the detached house and unit segments of the market, which is calculated as the ratio of mortgage repayments to gross average earnings of an individual (note that the average household earnings is are greater than the earnings of an individual in the vast majority of cases) on the purchase of a median price dwelling2. With the exception of the GFC period, affordability has shown rather steady improvement over the past decade. The eventual reversion to higher mortgage interest rates over the long term, however, is likely to put affordability under some pressure given that average housing debt levels are high by historic standards.

Shane Garrett is senior economist for HIA and can be contacted here.