Time to review pre-GFC yardsticks to judge future performance of commercial real estate: JLL's David Rees

GUEST OBSERVER

A new report by JLL says it is time to review pre - Global Financial Crisis yardsticks to judge future investment performance for commercial real estate. Instead, investors need to look more broadly at the long-term structural changes to the market that have been underway, behind the scenes.

And don’t wait for ‘normal’ market conditions to return, as traditional real estate benchmarks may not be reliable indicators in the future. Some metrics, such as workspace ratios and retail turnover ratios, may no longer even be relevant in the shifting world of workplace mobility and IT connectivity.

The Report - ‘Real Estate Conundrums - Just another cycle – or a whole new ball game?’ was presented at a JLL Research event in Sydney.

Technology and urbanisation have been gathering pace for decades. But while the cyclical nature of real estate has not been abolished, investors in real estate face a range of conundrums relating to yields, cross border investment, technology and urbanisation that can have long-term impacts for commercial real estate.

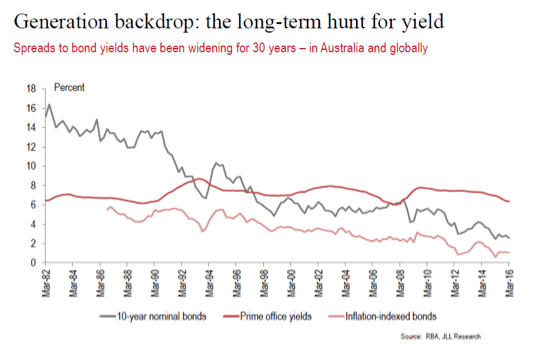

The GFC has been a convenient scapegoat for the breakdown in previously trusted rules of thumb when investing in commercial real estate. While for some the benchmarks of the years 2007-2008 do seem to mark a clear break from the patterns of the past, many trends have been evident for far longer than that. Not everything is a GFC-driven event. For instance, real and nominal interest rates have been declining for 30 years.

The challenge for investors right now is that numerous structural and cyclical shifts are emerging, converging and interacting with each other.

Structural shifts for Australian commercial real estate:

- Real estate markets are globalising – tenants, investors, developers

- Yields: Low growth, low inflation, low yields are also here to stay

- Cross Border Investment: Offshore capital is here to stay

- Fundamental mismatch between capital and available assets

Market cycles have not been abolished:

- Yields will cycle around lower benchmark levels

- Demography a key driver of all real estate asset classes

- Financial markets move faster than physical markets

- Don’t wait for ‘normal’ conditions to return

Structural Shifts – Yields and Cross Border Investment:

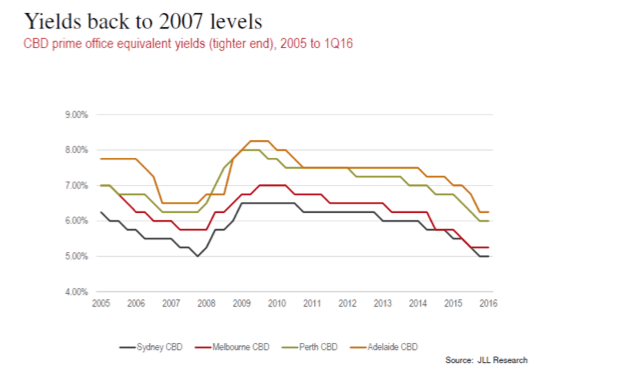

Implicit in JLL Research forecasts is a downward structural shift in interest rates and real estate yields – in other words, the ‘lower for longer’ theory is correct. This does not mean that cycles have been abolished. But average yields are likely to be lower than in the past.

Supported by growth in global pools of capital and a search for yield, JLL calculates that global cross border investment will continue to grow over the medium term. In Australia, cross border investors accounted for 42 percent of all commercial property transactions in 2015.

While the impact of technology has been massive, the impact on real estate has been less than was anticipated 20 years ago; CBD’s remain magnets for office and retail tenants, despite rising travel and congestion costs, and inner-city residential demand (which was not foreseen) has increased substantially.

Perhaps though the falling cost of technology, the advent of wireless capabilities, combined with the rising cost and scarcity of skilled labour and rising wages (that puts a premium on commuting travel times) will now lead to a more substantial impact on real estate investment returns and a re-ranking of market values in CBD and non-CBD locations?

If location premiums erode, non-CBD and suburban locations could be rewarding for investors.

Demography (and urbanization): – is it destiny?

Are we under-estimating the impact of the changing population age profile? Baby-boomers and first home buyers are important – but over time there are many other impacts on real estate to consider – childcare, student housing, retirement living as well as the age profile within the working age population.

While population will grow across all age categories in Australia, some age groups will grow much faster than others – therefore requiring specific real estate solutions – right across the spectrum from childcare, student accommodation, first home buyers, upgraders, empty nesters and retirement villages.

David Rees is regional director, head of research, JLL Australasia and can be contacted here.