Consumer sentiment shows modest March fall: Westpac's Bill Evans

GUEST OBSERVER

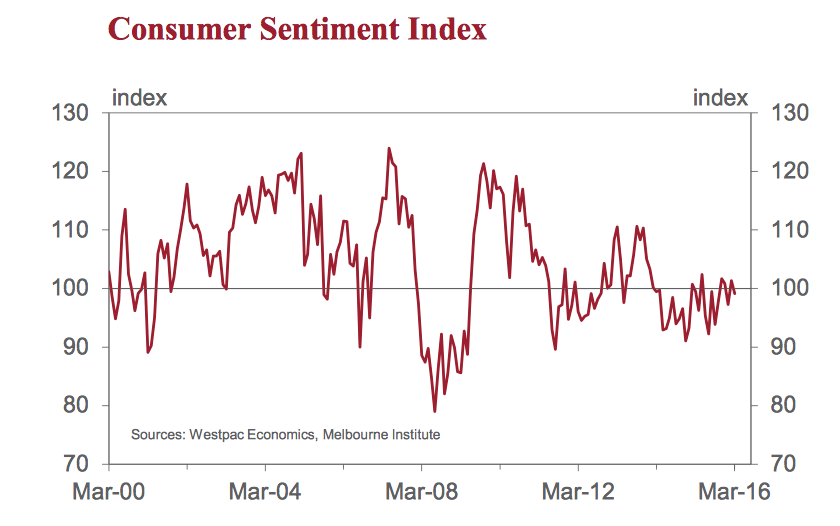

The Westpac Melbourne Institute Index of Consumer Sentiment fell by 2.2 percent in March from 101.3 in February to 99.1 in March.

The Index is back to around its average reading over the last six months. Following the change of leadership of the Federal Government in September the Index lifted by 8.3% over the subsequent two months. It has broadly held those gains with today’s reading off that high in November by 2.5% although we are now slightly back in the region where pessimists outnumber optimists.

Financial markets have maintained significant volatility since the last survey while finishing the month on an encouraging high.

However, responses to additional questions on ‘news items recalled’ indicate that consumers were generally less focussed on international events than in December. The proportion of respondents who reported recalling news on ‘international conditions’ fell from 20.0% in December to 15.5% in March although perceptions of this news remained highly unfavourable.

The highest levels of news recall were for items on ‘budget and taxation’ ( 37.1%) and ‘domestic economic conditions’(36.7%). Perceptions of both topics were less unfavourable in March than in December. Respondents registered low recall rates on new on ‘interest rates’, ‘employment’ and ‘inflation’ although again perceptions were significantly less unfavourable than in December.

However, the market volatility and unfavourable media coverage on property markets appears to have triggered a reassessment of risk preferences. When we asked consumers about the ‘wisest place for savings’ there was a much higher proportion nominating ‘pay down debt’ – 24.4% in March compared to 17.8% in December – with this month’s reading the highest since December 2011( 26.6%) when the European Financial Crisis was in full swing. This move to more risk averse preferences also saw a 4.5 percentage point increase in the proportion of respondents who favoured fixed interest investments, including bank deposits with significant reductions in the proportion nominating real estate (down to 14.7% from 23.4% in December ) and shares (down from 9.9% in December to 7.6% in March).

The Westpac Melbourne Institute Index of Unemployment Expectations increased by 1.3% from 145.3 in February to 147.3 in March. This measures respondents’ assessments of the outlook for the unemployment rate so an increase indicates reduced confidence in the employment outlook. The measure is still 5.8% below its print in September but has steadily lifted (up 9.2%) from the low in October (134.9). However labour market expectations are still considerably less negative today than they were through most of 2014 and 2015.

Three of the five components of the Index fell in March. One of the two components assessing family finances – ‘family finances compared to a year ago’ – declined 8.2%. The Reserve Bank has indicated that it favours this component as a reliable indicator

of spending intentions. As such, it would be of some concern that this component, which unlike the overall Index did not lift significantly following last year’s leadership change, is now down 5.9 percent from a year ago, a considerably weaker read than the 0.4 percent decline in the overall Index. The prudent approach to this sharp move will be to assess the degree to which it is sustained over future months.

The other family finances component – ‘family finances over the next 12 months’ – increased by 0.2 percent. The components measuring the views on the economic outlook sent conflicting messages – ‘economic conditions over the next 12 months’ increased by 8.2 percent while ‘economic conditions over the next 5 years’ fell by 2.5 percent.

The final component, ‘time to buy a major household item’ – fell by 6.6 percent to be 2.5 percent below its level from a year ago.

While there was a sharp deterioration in respondents’ views on real estate as a wise investment relative to December, assessments of ‘time to buy a dwelling’ suggest broader buyer sentiment may be stabilising. The ‘time to buy a dwelling’ index increased by 5.4 percent from 99.3 in February to 104.7 in March.

This Index is now 3.0 percent above its level in September but still 13.1 percent below its level of a year ago. The divergence between this index and views on real estate as an investment may reflect uncertainty around potential changes to taxation policy affecting negative gearing. Notably, the state detail on ‘time to buy a dwelling’ shows buyer sentiment in NSW – the weakest state – is now 44 percent above its September low although it is still 19 percent below its level from a year ago.

This stability is also indicated by the Westpac Melbourne Institute Index of House Price Expectations. The Index lifted by 9.8% in March to be 16.6% higher than its level in December although still 18.4% below its level from a year ago.

The Reserve Bank Board next meets on April 5. As we have been successfully arguing since June last year that we expect the Bank will keep rates on hold through 2016. Clear issues for the Bank will be the progress towards stability in the labour market and the value of the Australian dollar.

Recent dollar strength has been associated with a more positive outlook for China and commodity prices and as such would not be grounds for a policy adjustment.

Equally, while most indicators, including our own, one of which is quoted in this survey, point to an overall improvement in the labour market over the last six months, actual jobs growth appears to be running ahead of those indicators. The recent lift in the recorded unemployment rate to 6.0% seems consistent with that observation.

Given the recent GDP report showing Australia grew by a relatively impressive 3% in 2015, the current unemployment rate is a long way short of a print that would prompt a policy response from the Bank.

We expect growth in the Australian economy of 2.8% in 2016 with the genuine prospect for some stability in our terms of trade through the year laying a foundation for a lift in incomes and spending going into 2017.

Bill Evans is chief economist of Westpac.