House prices and debt pose significant risks without the RBA exacerbating them: Alex Joiner

It would however more than likely add further momentum to the property market and expansion of household leverage, according to Merrill Lynch economist Alex Joiner.

"It is our view that future risks outweigh any benefit especially when we consider any future tightening cycle," he said.

"Future risks will define any tightening cycle.

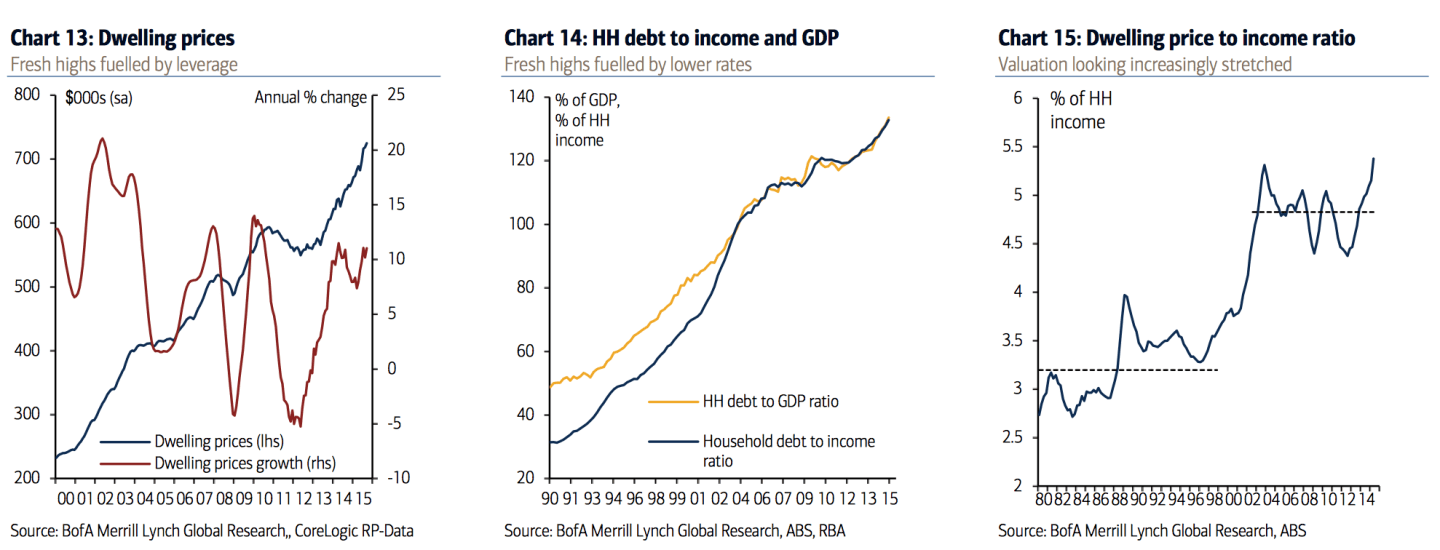

"Indeed, we already think that the level of dwelling prices and household debt pose significant future risks to the economy without the RBA exacerbating them with even lower interest rate settings.

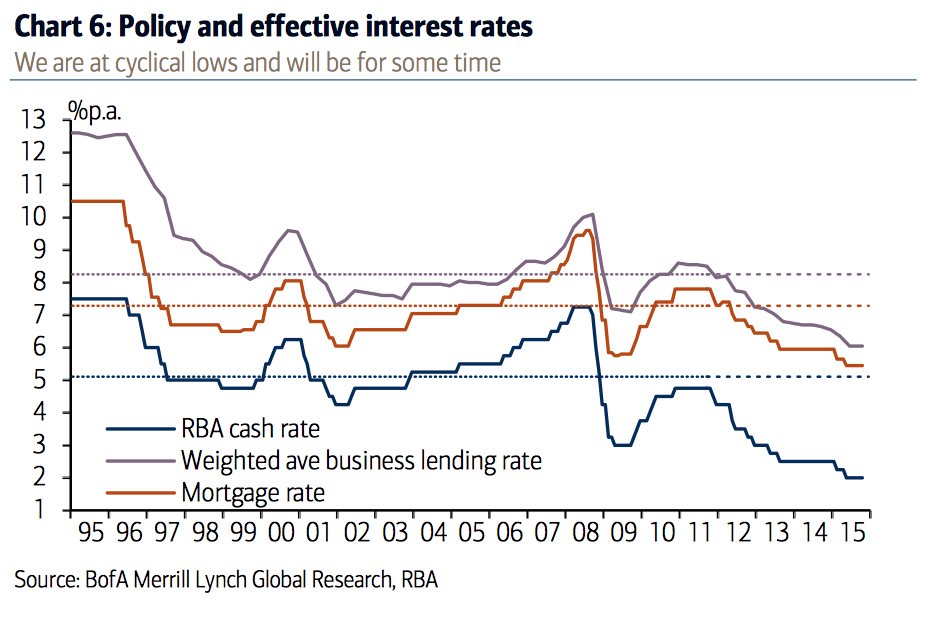

"And because of this, we think the balance of downside risks in the economy will increasingly transition from the business sector to the household sector. This is especially true when the RBA eventually does raise rates from what are record ‘emergency’ lows.

It would however more than likely add further momentum to the property market and expansion of household leverage.

"It is our view that future risks outweigh any benefit especially when we consider any future tightening cycle.

"Future risks will define any tightening cycle.

"Indeed, we already think that the level of dwelling prices and household debt pose significant future risks to the economy without the RBA exacerbating them with even lower interest rate settings.

"And because of this, we think the balance of downside risks in the economy will increasingly transition from the business sector to the household sector. This is especially true when the RBA eventually does raise rates from what are record ‘emergency’ lows.

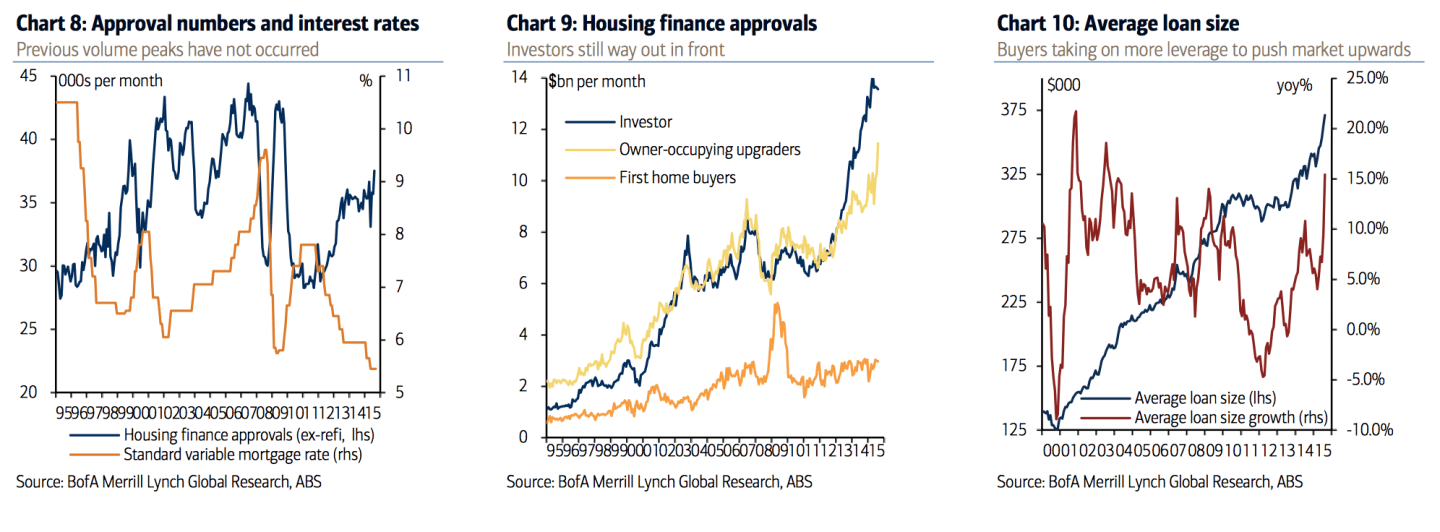

Joiner reckons the RBA decision making or lack thereof has arguably encouraged asset price inflation, household debt accumulation and almost inevitably speculative activity in the property market.

"In our view, the RBA and prudential regulators have been too cautious in its treatment of the property market in this easing cycle.

"It seems clear to us that stronger macroprudential measures should have been put in place significantly earlier than the ‘soft’ measures that are currently in place.

"And now, we think it may be a case of too little too late.

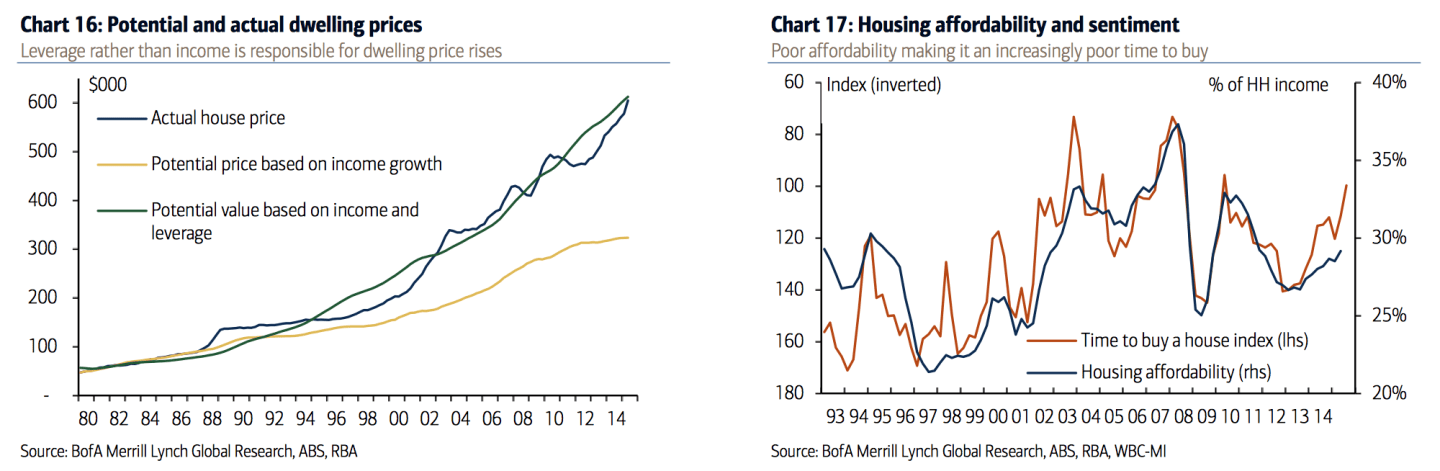

"In hindsight, it may have been worth it for the RBA to sacrifice some of the positive dwelling price impact on consumer spending and residential construction in order to reduce future risks (and potentially elongate cycles).

"Our analysis suggests that dwelling prices growth will decelerate markedly by the end of 2016 to be at or around the pace of income growth.

"Yet once the rate tightening cycle has begun, we would expect house prices to be 5-6% lower by the end of 2017.

"China is not the only hard landing risk in town.

"The scenario that is our base case, outlined above, looks for a modest but not detrimental decline in dwelling prices that will weigh on growth.

"We are not forecasting collapse or the bursting of any perceived bubble.

"That said, it is not difficult to envisage a more ‘hard landing’ scenario in the property market.

This would clearly have a greater negative macro-economic impact channelled through households and the residential construction cycle.

"A recent investor trip highlighted such an event as a key concern for clients across all asset classes along with a hard landing in the Chinese economy.

"We highlighted recently that the latter is a low probability, high impact, event that would be difficult for policymakers to manage.

"A disorderly decline in dwelling prices is a greater risk in our view and would be equally high impact and difficult to manage.

"It could come from a number of sources: households; investors; inadvertently from the RBA itself; or a combination of all three.

"Clearly the RBA will be closely watching dwelling prices as it eventually tightens policy.

"At best, we will escape with some cyclicality in dwelling prices that has little material impact on the broader economy.

"At worst, a hard landing that could represent a marked setback for the economy in coming years," Joiner advised.