Trouble looms, so rates should hold: Timo Henckel

GUEST OBSERVER

Wild swings in global stock markets have made investors edgy, the economic news coming out of China is not favourable and domestic private investment has plummeted. On the other hand, US growth surged to 3.7% annually and fears of a debt crisis in the Euro zone have abated. Latest estimates still put inflation at 1.5%, below the Reserve Bank of Australia’s target band of 2-3%.

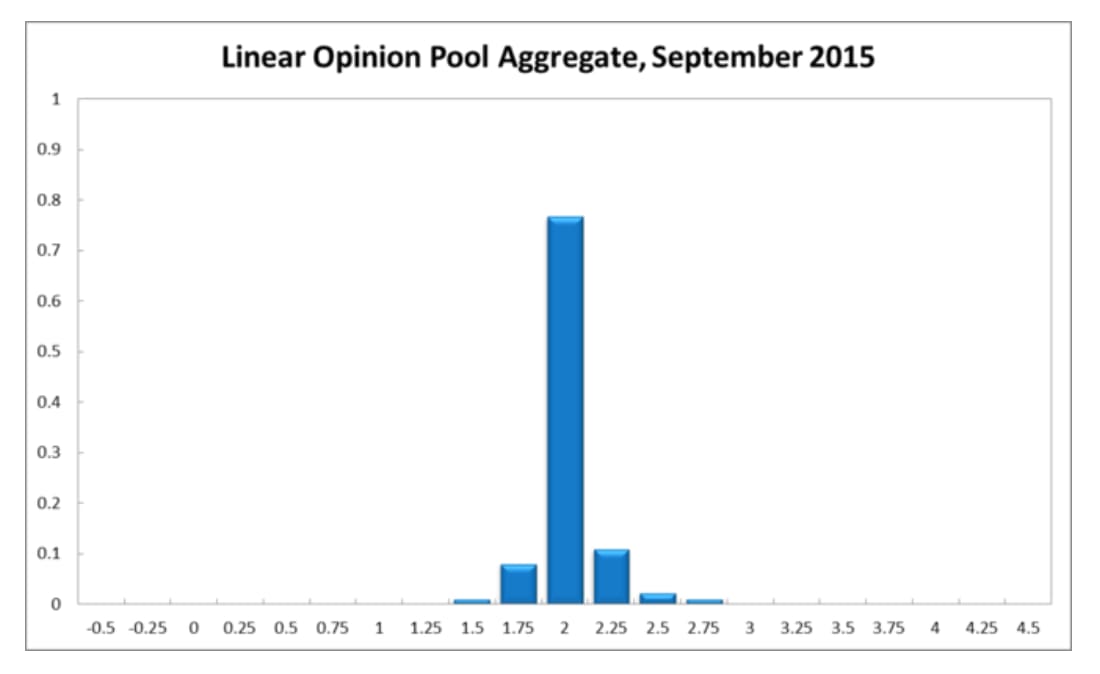

The Shadow Board’s confidence that the cash rate should remain at its current level of 2% equals 77% (up from 68% in August). The confidence that a rate cut is appropriate has edged up three percentage points, to 9%; conversely, the confidence that a rate increase, to 2.25% or higher, is called for, has decreased considerably for the third time in a row, from 35% in July and 25% in August to 14%.

Latest figures show that Australia’s unemployment rate increased to 6.3% in July, according to the Australian Bureau of Statistics, even though total employment rose by nearly 40,000 in July. Nominal wage growth remains muted at 2.3% and is forecast to remain low in the next quarter.

The Aussie dollar depreciated further against major currencies. It now fetches less than 72 US¢. Yields on Australian 10-year government bonds remain low at 2.71%.

As already pointed out in last month’s statement, the Australian property market appears to be cooling and the local sharemarket is retreating further from its highs earlier this year.

The elephant about to enter the room is the dramatic fall in new private capital expenditure, equalling a sizable 4.0% in the June quarter, bringing the annual decline to 10.5%, the largest drop since the last recession in 1992. The large drop is largely attributable to the contraction of the mining sector; however, firms in other sectors are also planning to cut spending, posing a serious threat to the Australian economy.

The recent gyrations in worldwide stock markets have highlighted the frothiness in global asset prices. To what extent volatility and uncertainty in asset markets spills over into the real economy is, of course, unclear. However, few economists doubt that asset markets are relying on ultra-low interest rates to persist. Concerns about any debt crisis in the Euro zone have waned since the recent 80 billion Euro credit extended to Greece.

As in previous months, the deteriorating outlook for the Chinese economy pose the biggest immediate threat to Australia’s export markets and thus to Australia’s GDP. US growth, on the other hand, has been revised up to 3.7% (annualized) for the second quarter 2015, presenting a dilemma for the Federal Reserve Bank: the strong economic performance suggests an increase in the federal funds rate is around the corner but if volatility in stock markets persists, signalling heightened uncertainty about the future, the Fed may be tempted to postpone the interest rate increase. Commodity prices have continued to fall, with crude oil dipping below $40 a barrel.

Also of concern is the sizable contraction of world trade in the first half of this year. The volume of global trade shrank by 0.5% in the June quarter, while the figures for the March quarter were revised to a 1.5% contraction, indicating that world trade recorded its largest contraction since the 2008 global financial crisis.

Consumer and producer sentiment measures paint a motley picture. The Westpac/Melbourne Institute Consumer Sentiment Index jumped from 92.3 in July to 99.5 in August. Business confidence, according to the NAB business survey slumped from 10 in July to 4 in August, at the same time as the AIG manufacturing and services indices, both considered leading economic indicators, recorded notable improvements.

What the Shadow Board believes

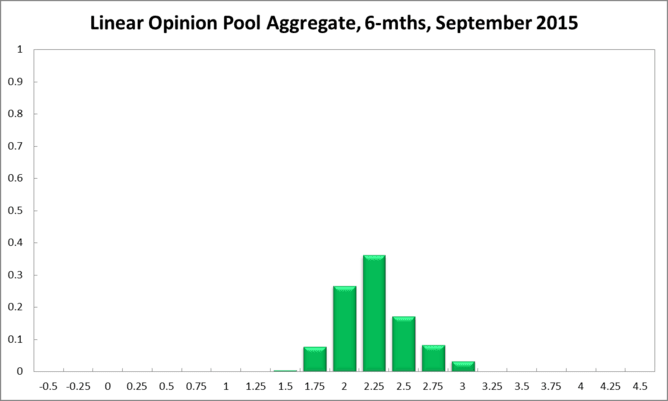

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 2% equals 27% (23% in August). The estimated need for an interest rate increase lies at 65% (73% in August), while the need for a rate decrease is estimated at 8% (4% in August).

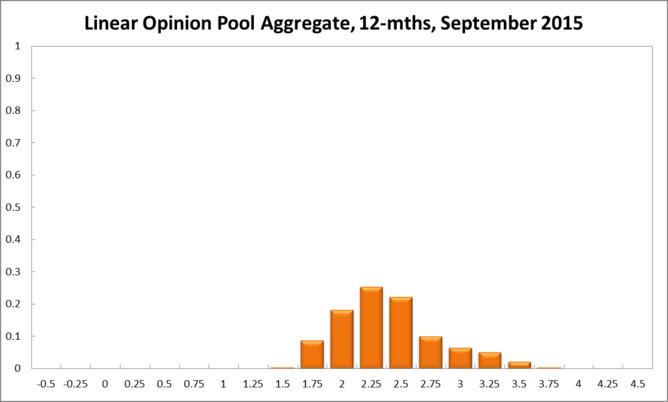

A year out, the Shadow Board members’ confidence in a required cash rate increase equals 72% (six percentage down from August), in a required cash rate decrease 9% (7% in August) and in a required hold of the cash rate 18% (up from 15% in August).

Comments from Shadow Board members

Mark Crosby, Associate Professor, Melbourne Business School:

“The longer term outlook is still uncertain.”

Recent global gyrations should make the RBA hold rates this month, and with a recovery in equity markets outside of China there seems little reason to cut rates. The longer term outlook is still uncertain, with global trade falls the most recent worrying data in the global economy and far more consequential than falls in Chinese equity markets.

Guay Lim, Professorial Fellow, Deputy Director, Melbourne Institute:

“International interest rates are likely to rise.”

International interest rates are likely to rise, as growth and employment in the US appear to be stabilising at normal rates. While Australian asset markets are expected to continue to be volatile, the exchange rate is expected to remain low. Keeping the official rate steady at 2% would help offset some of the negative effects of uncertainty in the international environment on the domestic economy – as well keep the policy rate well above the zero lower bound.

James Morley, Professor of Economics and Associate Dean (Research) at UNSW Australia Business School:

“The RBA should not provide a ‘Greenspan put’.”

Given the recent turbulence in financial markets and underlying inflation being at the low end of the target range, the RBA should hold its policy rate steady rather than raise it. But with a stable real economy, an overheated housing market, and a low dollar stimulating the foreign sector, the RBA should not provide a “Greenspan put” by cutting rates in response to the stock market. Instead, it should carefully monitor conditions to determine when it will need to start raising the policy rate back towards its neutral level.

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

“Monetary policy needs to avoid reversing recent currency falls.”

The current fragility in global stock markets appears to be more of a dash to liquidity than to value. It is likely an over-reaction to expected future interest rate increases, beginning with the federal funds rate perhaps this year. Nevertheless some downward adjustment was probably necessary because the boom in global stock prices generally did not mirror the sluggish recovery in the global real economy.

The trade-weighted Australian dollar has fallen about 15% in the last year, and fortunately has not risen with the recent competitive depreciations across Asia. Monetary policy needs to avoid reversing this contributor to Australia’s improved export competitiveness. In the current volatile financial environment, the RBA should maintain the current cash rate in September, though I have modestly increased the probability of a desirable cut.

esearch associate, Centre for Applied Macroeconomic Analysis at Australian National University and author for The Conversation. He can be contacted here.